THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

Budgeting can be complicated, and it’s easy to fall into bad budgeting habits without noticing the problem.

Budgeting can be complicated, and it’s easy to fall into bad budgeting habits without noticing the problem.

Budgeting mistakes can make it much more difficult to reach your financial goals, so it’s important to identify any issues that could be holding you back.

Everyone’s budgeting experience is different, but there are a number of typical errors that you may not be aware of.

This article will cover a few of the most commonly overlooked budgeting mistakes and how you can adjust your approach to fix them.

Table of Contents

5 Way To Fix A Budget That Doesn’t Work

#1. You’re Being Too Strict

It’s good to take budgeting seriously, but being overly tight with spending can actually have a negative effect.

Trying to cut out things like entertainment and hobbies will only make you resent your budget, and you’ll be more likely to ignore your financial goals by making an impulse purchase.

How to fix it: Include leisure costs in your budget.

While there’s nothing wrong with trying to reduce how much you spend on things you don’t need, that doesn’t mean you should go too far in the opposite direction.

Be realistic about how much you want to spend on fun, and try not to let yourself feel bad about having a good time.

Begin by looking through previous bank statements to track how much you usually spend on these costs.

From there, you can determine whether you’re content with your existing habits or need to make an adjustment.

If you do decide to start spending less, aim for small, gradual changes rather than changing your lifestyle immediately.

#2. You’re Only Budgeting For Minimum Payments

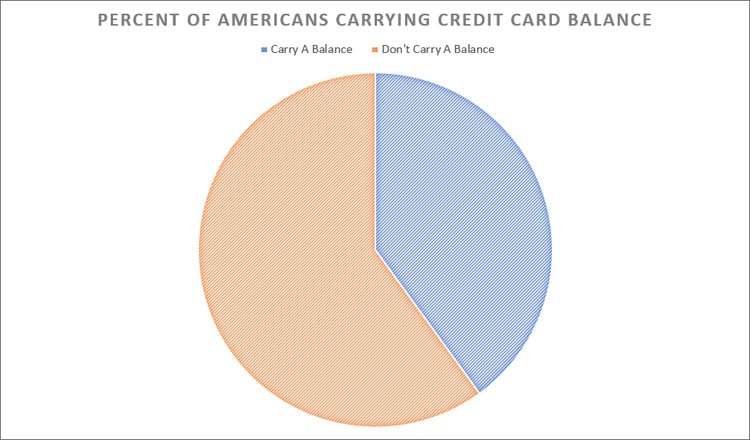

Nearly 40% of American households carry a credit card balance from one month to the next, and they might not consider this debt an important financial concern.

“I’ve made the minimum payment, so I’m good, right?” is the general thought process.

The truth is that credit cards usually come with extremely high interest rates compared to other forms of credit, and over time, the interest accrual will kill your budget.

Paying off debt isn’t an exciting way to use the extra money in your paycheck, but the balance will only continue to grow if you don’t start making payments.

The average credit card interest rate is over 14% for existing accounts and more than 19 percent for new accounts.

How to fix it: Increase the amount you budget for credit card payments.

You might feel overwhelmed by your credit card balance and other debts, but you can start moving toward becoming debt-free by putting as much as you can toward them.

Since debts grow the longer the balance remains unpaid, they should always be one of your top financial priorities.

If you’re currently managing multiple debts, start by paying down the balance with the highest interest rate before moving to the lowest.

This is the most efficient way to get out of debt while avoiding as much interest as possible.

#3. You’re Using Somebody Else’s Budget

If you can’t connect your budgeting habits to real-life goals, it will be tough to stick to your budget when you have no motivation.

When you’re simply choosing between an arbitrary budget (perhaps one you found online) and something you really want, there’s a good chance you’ll give yourself the immediate satisfaction.

You need to connect your budget to real, actual goals.

Why are you going through this monthly exercise of budgeting and sticking to it? You need to write down exactly why you’re doing this.

And of course, vague or generic goals probably won’t help you stay motivated.

Some people try to “save money” without committing to anything specific, but this isn’t usually an effective long-term approach.

How to fix it: Define your short and long term goals.

Budgeting is almost always beneficial, but it’s easier to stay committed if you’re targeting both short and long term financial goals.

Rather than spending less just to be more frugal, you’ll be moving toward a tangible goal like starting to invest, saving for retirement, or building a college fund for a loved one.

For the same reasons, it’s best to come up with a concrete, measurable goal each month.

Start with something small, even just $25 or $50 per month will go a long way.

When you’re tempted by something you don’t need, keep both your immediate and long term needs in mind.

It’s easier to hold off when you believe the money you save is going to something more important.

#4. You Don’t Include Unexpected Costs In Your Budget

It’s easy to budget for recurring and regular expenses like groceries, subscriptions, and gas, but things get more complicated for new or one-time costs.

If you need to go to the dentist and take your cat to the vet in the same month, you’ll find yourself going over budget quickly.

When unavoidable expenses completely change your budgeting plans, it can be tough to get back on track.

In order to budget effectively, you’ll need to maintain a long term outlook that takes costs into account before they come up.

This will help you avoid financial surprises and stick to your budget without breaking the bank for major expenses.

How to fix it: Build an emergency fund and budget for surprises.

With an emergency fund, you’ll be able to cover unexpected costs that would otherwise derail your budget.

Once you’ve saved enough money, your emergency fund will also be your first fallback if you lose your primary source of income.

Many experts therefore recommend building a fund equal to at least three months of expenses.

It will take time to reach that goal, but just a few hundred dollars will help you get through a range of difficult financial situations.

Even if you’re currently in debt, it’s still a good idea to put at least some of your paycheck toward an emergency fund if you don’t already have one.

Just as an emergency fund gives you some insurance for surprise expenses, you can budget for the costs you are expecting by starting to think about them a few months in advance.

If your ten year anniversary is coming up, for example, don’t wait until that month to budget for the cost of a gift.

Instead, identify it as a future expense around six months in advance, then divide the cost and save a fraction of the total each month.

Rather than budgeting for $300 all at once, for example, you can start taking $50 out of your paycheck six months beforehand and distribute the savings more evenly.

If the seller offers financing with little or no interest, take advantage of this option to give yourself even more time to pay off the debt.

If you know you’ll have six months to make payments, for example, you could divide that initial $300 into twelve payments of just $25.

The more you can spread out these costs, the easier it becomes to account for them in your monthly budget.

#5. You Ignore The Small Stuff

When you first started budgeting, you probably focused on the largest and most obvious expenses.

It’s satisfying to save a lot of money with a single change, and this is undoubtedly the simplest way to budget.

On the other hand, when you prioritize your most expensive purchases each month, it’s easy to forget how quickly the smaller things add up.

You could be spending a lot less (and taking some pressure off of other changes) by regularly reviewing the less conspicuous areas of your budget.

How to fix it: Review your statements every month.

Most of us lose track of how much we spend on things like subscriptions, coffee, and nights out, but these are often the expenses that put us in financial trouble.

Rather than being satisfied with a few changes, make sure to thoroughly examine your bank statements at the end of each month to see exactly where your money is going.

If you’re having trouble staying on top of your budget, consider downloading one of the many free and low-cost mobile apps designed for users new to budgeting.

They’ll help you categorize your expenses, set up automatic payments, and make the best adjustments to start moving in the right direction.

Once you develop the habit of looking over your statements, you’ll start to get an idea of your most problematic spending habits.

From there, you can begin to develop realistic financial goals that match your current budget and long-term needs.

By evaluating your budget every month, you can adjust your goals based on lifestyle changes or results from the previous month.

Your budget shouldn’t be static. It’s important to consistently adapt your approach to your current financial circumstances.

Bonus: The Importance Of Accountability

Another option for you if you have trouble sticking to your budget is to ask someone close to you to check in on your progress and hold you accountable for your decisions.

Make sure this is someone you trust completely.

It’s important that they’ll tell you the truth if things aren’t going well.

With an accountability partner, you won’t be able to shrug things off if you miss your targets.

In the same way that an exercise partner can help you keep making progress even when you aren’t motivated, accountability partners give you another reason to stick to your budget.

Final Thoughts

Budgeting is the best way to build better spending habits, but many people give up on their budgets in the first few months.

These tips will help you develop realistic expectations and create the budget that’s right for your income, expenses, and financial goals.

Remember to check your statements every month to look for even more ways to save money.

Author Bio: Logan is a CPA, personal finance expert, and founder of the finance blog Money Done Right, which he launched in July 2017. After spending nearly a decade in the corporate world helping big businesses save money, he launched his blog with the goal of helping everyday Americans earn, save, and invest more money.

I have over 15 years experience in the financial services industry and 20 years investing in the stock market. I have both my undergrad and graduate degrees in Finance, and am FINRA Series 65 licensed and have a Certificate in Financial Planning.

Visit my About Me page to learn more about me and why I am your trusted personal finance expert.