THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

I’ve heard all of the excuses.

I’ve heard all of the excuses.

Understanding your finances is hard.

You don’t know who to trust.

You’ll get to it tomorrow.

I could write over 100 excuses in a few minutes.

And they are all excuses, plain and simple.

The truth is, financial planning isn’t hard. It does take some work on your part, but you can easily do it.

And this post is here to help.

I am going to list out the 10 most critical financial tips to help you be better financially.

Think of it as a step by step financial planning guide.

By the time you are done, your finances will be on solid ground.

No more making excuses. No more worrying if you can retire.

You will have done the most important things to improve your finances over the long term.

Let’s get started with the 10 financial planning tips you need to tackle right now.

10 Financial Planning Tips To Make Your Money Last

#1. Life Insurance

Surprised this is #1?

If I didn’t know better, I would too.

But here is the thing.

I worked at a financial planning firm that only dealt with wealthy clients. And the #1 mistake they were making is the same mistake you are making.

Not having life insurance.

Our clients overlooked insurance because it is boring. They focused more on the sexy parts of their finances, like their investments.

But trust me when I tell you that not having proper insurance coverage can crush you.

And it can do so in an instant.

In one case, we had a client who passed away suddenly without life insurance. His wife hadn’t worked for years, raising their children.

Suddenly, she was without a partner and without an income.

Not only did she have to deal with the grief of his passing and plan the funeral, but she also had to find a job.

This meant creating a resume, looking for open positions, interviewing, etc.

Her entire life was through upside down.

Had her husband had life insurance, some of this could have been avoided.

She still would grieve and plan the funeral, but she wouldn’t need to find a job right away.

The life insurance proceeds would have helped out tremendously.

Your Action Step

While the stats say we are going to live into our 70s, the truth is we all don’t.

And if someone relies on your income, you need to have life insurance.

Now I know life insurance can be tricky.

But here is the basics you need to know.

- Stick to term insurance. I find it is more affordable and doesn’t have hidden fees.

- Look at getting coverage for up to 10 times your annual salary. For example, if you make $50,000 look at a policy valued between $500,000 and $750,000.

- If someone relies on you or income, you need coverage. Don’t make the mistake of thinking a stay-at-home spouse doesn’t need coverage. If they pass, you need to find someone to care for the kids.

If you simply follow these guidelines, you will protect your loved ones in the event of your passing.

Where do you look for life insurance?

You could call up a bunch of providers, or you could use Bestow.

They make it easy by showing your quotes in one place.

Just enter in some basic information, and in seconds you can have a quote. If approved, you can have a policy under 10 minutes.

It’s so easy, there is no reason why you can’t do this right now and check this one off your list.

In fact, do it right now. Then come back and finish up this post.

#2. Disability Insurance

I know what you are thinking, another point on insurance?

Disability insurance is critical and yet even fewer people have this coverage than life insurance.

The scary part is you are more likely to get disabled than you are of dying prematurely.

In fact, 25% of today’s 20 year olds will become disabled before they retire.

To help you understand why disability insurance is important, I have another client story for you.

We had a client whose daughter slipped on a patch of ice in her driveway one morning. She was 29 years old.

She hurt her back and was out of work for 6 months.

While she has returned from work, she is only working part time because of the frequent doctor visits and therapy sessions she attends.

She went from making $70,000 a year to making $20,000.

Talk about a life changing event.

While disability insurance won’t make up the entire difference of lost wages, it will soften the blow.

Your Action Step

Price out disability coverage.

It is something no one ever talks about but is more likely to happen to you.

You can get a free quote from Breeze in seconds and tailor your policy to your exact needs.

Even I was guilty of this skipping this one.

Then my manager at the planning firm convinced me otherwise.

Don’t make the mistake of thinking it can’t or won’t happen to you.

Click on the link to Breeze above and get yourself covered.

#3. Create A Plan

OK, enough talk about insurance!

The next step to financial success is to have a plan.

But not just any plan.

You need a detailed plan for your life.

Take the time to figure out what you want out of life.

- What are your goals?

- Do you want to travel?

- What is your ideal job?

- What does retirement look like?

Think about these and other questions to get a complete understanding so you can create a plan to achieve everything.

For example, maybe your ideal job is working at a non-profit helping abused pets.

And maybe you only want to work 20-25 hours a week because you also want to foster animals, so you want to be able to spend time at home with them.

By having a plan, you can save and budget so this dream becomes a reality.

Your Action Step

Take some time to think about your dreams and write down your goals.

In the beginning, just take notes about whatever you are thinking. Don’t judge at this point, just write down everything that comes to mind.

Do this for a couple days and then forget about it.

Come back a few days later and reread through your notes.

Which ones resonate with you? Circle these as they are your true goals.

Cross off the ones that don’t resonate.

Then start building on the goals you set.

This mean write specific details about the goal. The more specific you are, the more likely you will take action on them.

You won’t be able to complete your plan at this point, but as you keep reading the following tips, you will have the information you need to complete it.

#4. Know Your Spending Rate

How much money do you spend a year?

Most people, and by most I mean 99%, have no idea.

They could take a guess, but the majority of people underestimate.

For example, when I was coaching people to improve their finances, I would start out by having them take a guess.

Then we would figure it out. And every one that guessed, spent more than they thought.

When they saw the actual number, they couldn’t believe it.

In fact, many tried to argue that it wasn’t possible. But when I asked them to show me where the money is, like in a savings account, they couldn’t.

They admitted they spent this amount.

By knowing how much you spend, it can have a drastic impact on your finances.

Many people will instantly start saving more and cutting expenses.

Your Action Plan

Take some time, like right now, to figure out how much you spend.

There are a few ways you can do this.

Credit Card Statements

First, if you mainly shop using credit cards, just log onto your credit card website and get your annual spending summary.

Most offer this, but if yours doesn’t, just download each monthly statement and total up the spending.

While this method isn’t 100% accurate, it does give you a ball park number.

Ballpark It

This way isn’t the best, but it is quick and gets you a rough idea.

Write down all of your major monthly expenses and total them up.

Then write down all of the smaller monthly expenses you have to get a complete picture.

Next, multiply this number by 12 to get an annual number.

Most people will forget about non-monthly expenses, so be sure to include expenses that aren’t monthly charges, but still add up.

This includes:

- Insurance premiums

- Seasonal expenses like landscaping or maintaining a swimming pool

- Gifts

Add the total of these to your annual spend number.

Finally, add 10% to this number because there are expenses you are forgetting about.

Tax Return

This one is my favorite, but it takes more work and some math.

I like it because it is the most accurate estimate out there.

To use this method, you need last year’s tax return, a sheet of paper, and a calculator.

Having the tax tables from last year is needed as well.

I am not detailing the process here, as I have a complete walk through of this process in the post below.

By using this method, you will get the most accurate estimate of how much money you spend.

Then with this information, you can start to make adjustments to spend less and save more.

Even by decreasing your monthly spending by 5%, it will have a dramatic impact on your finances.

#5. Pay Off Debt

This one is a no-brainer, but needs to be listed.

In order to reach your financial goals, paying off your debt is important.

Here is a quick example of why.

Let’s say you need $50,000 a year to live.

Of this amount, $750 a month is used to pay various loans.

When you look at this number on an annual basis, you need $9,000 of income just to pay this debt!

The bottom line is debt handcuffs you when it comes to not only achieving your goals, but even in taking advantage of opportunities that come your way.

For example, let’s say you are offered a job caring for animals. The catch is it pays $40,000 a year.

Because of your debt, you can’t take this awesome job.

But if you didn’t have debt, you could take the job.

Your Action Plan

You need to make it a priority to pay off your debt.

You can read through the debt articles on my site for help with paying off debt, including motivational tricks and plans.

You should also check out the building wealth articles as well.

There you can find ideas to make money on the side to help you pay off your debt faster.

- Read now: Click here to get help paying off your debt

- Read now: Click here to learn the best tips and tricks to build wealth

By making it a priority to pay off debt, you can take advantage of opportunities that come your way.

#6. Enjoy Today

While getting out of debt is a priority, it shouldn’t be so important that you miss out on today.

I’ve made this mistake and it wasn’t fun.

Back when I was in debt, I wanted to pay it off super fast.

So I took every extra penny I had and used it to pay down my balances.

The problem was I didn’t have any fun money. No going out with friends. No seeing movies or concerts.

Nothing.

It wasn’t a problem at first because I wanted to get out of debt.

But I didn’t want to get out of debt so fast that I couldn’t spend time with my friends.

I adjusted my plans and set some money aside to enjoy life while still paying off my debt.

In all, it took me a little over a year to get out of debt.

Looking back, I can’t say I would have paid off my debt any faster if I put every penny towards my debt.

This is because at some point I think I would have broken down completely and focused all my attention on spending time with my friends and ignored my debt.

Your Action Plan

Find a healthy balance when it comes to saving for tomorrow and living life today.

It is not an all or nothing decision.

You can easily do both.

You just have to find the balance that works for you.

When you find what you think is your balance, try it out for a few months and see how you feel.

If you are happy, keep going.

If you find you are not happy, then figure out a new balance and try it out.

Eventually you will find the balance that works for you.

#7. Focus On Savings Not Return

One of the easiest ways to be better financially is to save money.

Unfortunately, most people don’t save anything.

Of the ones that do save, they focus on their return and not their savings rate.

The truth is, your savings rate is much more important than your return.

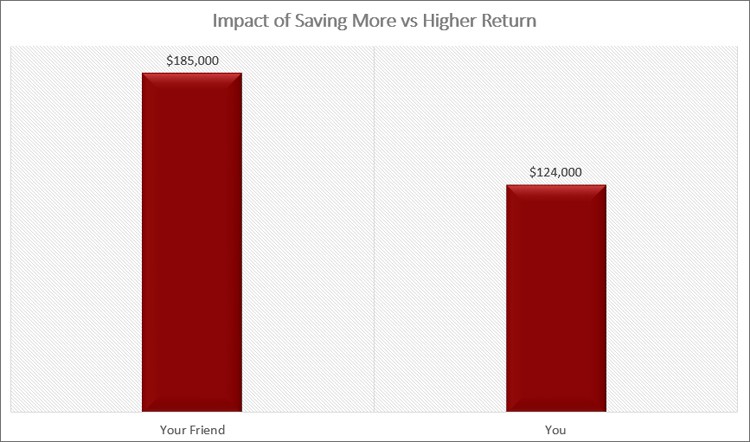

For example, let’s say your friend makes $50,000 a year and saves 15%, which is $7,500. They earn 2% interest in their savings.

You save $2,500 a year but you make earning as much money on your savings a priority. You earn 8% on your money.

If you both keep saving the same amount and earning the same returns, who has more money in 20 years?

Your friend ends up with close to $185,000. You have nearly $124,000.

That is a difference of $60,000!

The point is, you need to save as much money as you can.

Stop worrying about your return and start focusing on ways to save as much as possible each month.

Your Action Step

The easiest way to start saving is to automate your savings. By making it automatic, you don’t have to remember to save.

It just happens every single month.

Another smart thing to do is to save first.

Too many people try to save what is left at the end of the month.

Start saving when you get paid, then spend the rest.

I use CIT Bank to save money. They make it simple to automate my savings and I don’t to worry about a thing.

Click here to open your CIT Bank account today

#8. Invest

I know I just told you that you need to focus more on your savings rate than your rate of return.

But you cannot completely ignore your rate of return.

If you just put money into a low interest savings account, your odds of reaching your financial goals are much harder than if you invest.

Let’s take the above example again, but this time extend the time period to 40 years.

In this case, your friend ends up with close to $460,000. You end up with roughly $700,000.

That is $240,000 more!

The point here is that you need to invest your money.

By earning a higher rate of return over longer periods of time, you make the odds more likely that you will reach your goals.

Your Action Plan

I know investing can be scary for some of you.

But I have a solution.

It is called Betterment.

They are a robo-advisor that automates investing for you.

All you do is answer a few questions about your goals and investment timeline and Betterment will create a portfolio for you.

All that is left for you to do is to set up a monthly investment.

Just sit back and let your money start working for you.

Click here to get started with Betterment

#9. Get Your Documents In Order

The next area to work on when it comes to getting in shape financially is to make sure you have all of your documents.

There are a handful of important papers you need should something happen to you.

- Will

- Living Will

- Health Care Directive

- Medical Power of Attorney

In addition to these, you want to make sure you have beneficiaries listed on your investment accounts.

This will make the process of transferring the accounts to your heirs that much easier.

Your Action Step

Take the time to get these documents prepared.

While they will take a little time when you meet with an attorney, the time spent is more than worth it.

And the price you pay depends on many factors, including where you live and how complicated your life situation is.

When I created my first will, I was in my early 30’s and single. Because my life situation was simple, it only cost me a couple hundred dollars.

When I created a new will after getting married and having kids, the price increased a little, but not too much.

You might wonder why I created a will when I was single.

I did it so my loved ones didn’t have to worry about what to do with my belongings.

Everything was outlined for them. They could focus their energy on other things.

At the end of the day, it doesn’t matter if you are single or not. These documents are critical to have.

#10. Accept Life Happens

The final financial planning tip is to be open and accept that life happens.

Your goal of working with animals might change once you have kids.

Or your goal of golfing in retirement might change to travel.

The point is, life happens.

We can plan based on what we know today, but we have to be open and flexible in knowing that tomorrow things can change.

This isn’t to say because life happens you shouldn’t bother with improving your finances or creating a retirement plan.

While life does happen, having a plan will make navigating the changes much easier.

For example, even if you don’t want to golf in retirement but travel instead, having paid off your debt and saved as much as you can will only make this new goal that much more attainable.

I remember back when I started working after college and I wanted to earn extra money on the side.

The goal of this money was to help me retire as soon as possible.

But one day I lost my job.

The money I saved helped me to pad my budget in the short term.

During this time I took one of my hobbies and turned it into my main income.

Fast forward to today and this has allowed me to work from home and watch our daughters a couple times a week.

Life happened. My plans changed.

But by having a plan in the first place, it made the new goals a possibility and not a dream.

Your Action Plan

You need to be flexible with life and learn to roll with it.

Not everything you plan for will happen. And many things you never planned for will.

This is what life is all about.

The better you are at accepting this and reassessing your plans and goals as time goes by, the happier you will be.

I encourage you to review your goals and plans every few years.

Some times you will find nothing has changed.

Other times you will find that a goal you had is no longer a priority.

Whatever comes up, make adjustments and go from there.

Final Thoughts

At the end of the day, if you want to be better financially, you need to do follow these financial planning tips.

While you could hire a professional, you can do these things yourself.

It just takes time.

I encourage you to start the process by taking the first step.

Work your way through this list and be sure to review things every few years.

By doing so, you will put your finances on a firm foundation and will set yourself up for living a life of wealth.

Disclaimer: This post was made in paid partnership with Bestow. The opinions and ideas expressed in the article are those of the author(s) and are not promoted or endorsed by Bestow or North American.