THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

A critical part of investing is making sure your investments don’t get away from your initial asset allocation model.

This naturally happens over time as the market moves up and down.

But many investors overlook the importance of rebalancing their investment portfolio.

In this post, I share with you the importance of rebalancing as well as how to rebalance a portfolio.

While it might seem simple on the surface, if you rebalance incorrectly, you will cost yourself money.

How To Rebalance A Portfolio

What Does Rebalancing Mean?

Rebalancing means selling some overweight asset classes and buying underweight asset classes to get your portfolio’s risk level back to your target risk tolerance.

In other words, it simply means buying and selling your holdings to get back to the original mix when you started investing.

Why The Need To Rebalance Your Portfolio

As I mentioned, as the market moves, your portfolio over time gets out line.

Because of this, you need to reallocate your investments back to your target allocation.

But why is this necessary?

Here is a basic example.

Let’s say you determine your investment objectives and your risk tolerance and decide that a 60% stock and 40% bond portfolio is best for you.

- Read now: Here is how to figure out your risk tolerance

- Read now: Find a beginners guide to asset allocation

You invest $10,000 in total, so $6,000 goes into stocks and $4,000 goes into bonds.

Two years later, the stock market has gained in value and your balanced portfolio now is worth $18,000.

You have $12,600 in stocks and $5,400 in bonds.

On the surface, all looks good.

But if you look at these numbers as a percentage, you see that your portfolio is now weighted 70% stocks and 30% bonds.

It might not seem like an issue, but it is.

You are taking on more risk than you are comfortable with.

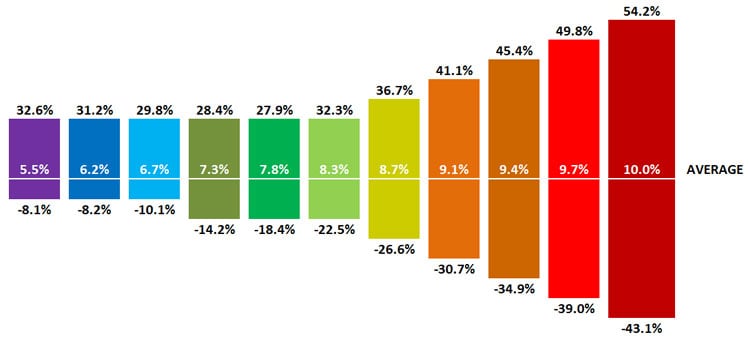

Look at the image below.

The mustard rectangle is the returns for a 60% stocks, 40% bonds weighted portfolio and orange rectangle to the right is a 70% stocks, 40% bonds weighted portfolio.

The middle number is your average annual return.

The top number the is best one year return and the bottom number is the worst one year return.

With your ideal portfolio the most you can expect to lose is 26.6% in a given year.

With the portfolio you are now in, you can expect to lose 30.7% in a given year.

Having a portfolio value of $18,000 that comes to a difference of close to $1,000 more in losses.

Reading that doesn’t sound scary.

But what if your portfolio grew to $200,000 in value?

Now the difference in possible loss is over $8,000 all because your asset classes are out of alignment.

And as time goes on, you will most likely move into a more stock heavy portfolio because stocks tend to outperform bonds.

In 10 years you might have a 80% stock and 20% bond portfolio.

If the market crashes, your $200,000 portfolio lost close to $70,000 or $16,600 more than if you were in your target asset allocation model.

Think for a minute how you might react to this market volatility.

You might get scared and sell out of the market.

- Read now: Find out how to handle a volatile stock market

- Read now: Learn how to invest when you are scared of the stock market

If you do, you lock in those losses.

Maybe you put your money into a savings account.

With interest rates low, you barely earn any money and as a result, never reach your financial goals.

The bottom line is, investing in the stock market is an emotional roller coaster and rebalancing your investment portfolio is critical for long term successful investing.

Let’s look at the best ways to rebalance your portfolio.

How To Rebalance Your Portfolio

There are a handful of ways to reallocate your portfolio back to the asset allocation strategy you created.

Here are the most popular ways.

#1. Sell Overweight Holdings

One of the easiest ways to get your portfolio back in balance is to simply sell over weight asset classes and use the money to buy underweight asset classes.

There is one major issue with this strategy and it is tax implications.

When you sell investments in a taxable account, you realize capital gains.

These gains, depending on if they are long term capital gains or short term capital gains are taxed.

So if you have to sell a lot of investments to get your portfolio correctly aligned, you might have huge capital gains taxes you have to pay.

The good news is that you don’t have to worry about taxes in your retirement accounts.

Your retirement accounts, like your 401k plan, Traditional IRA, or Roth IRA, grow either tax deferred or tax free.

- Read now: Find out the pros and cons of a Roth IRA

This means you can buy and sell whenever you please and not have to worry about taxes.

Another potential issue is when you are selling investments, particularly stocks, there might be transaction costs, making selling assets not an ideal option.

At the end of the day, this strategy works best for tax deferred accounts and for taxable accounts that don’t have a lot of money invested.

#2. Redirect Future Contributions

Another option is to simply redirect new investments.

You would use this in taxable accounts to avoid the tax consequences from capital gains.

When you invest new money, simply invest it into the under weight holdings until your portfolio is aligned.

Then you can invest as you were before you needed portfolio rebalancing.

The problem here is if your portfolio is out of balance by a lot, it might take a long time to get it back in sync with your goals.

#3. Direct Dividends To Under Weight Holdings

To help with the issue pointed out above, you can elect to redirect any dividends you earn.

An individual investor chooses to reinvest dividends back into the mutual fund or exchange traded fund they were earned from.

- Read now: See the benefits of dividend investing

Simply turn this feature off and have the dividends go into your cash account or money market account.

Then take that cash and invest it into your under weight holdings.

This will help you more quickly get back in balance when used with the idea of redirecting future contributions.

However, in some cases, your dividends might be small, not speeding up the process as much as you might like.

#4. Look At Your Investments As A Whole

Finally, you can choose to look at all of your investments as one, as opposed to individual portfolios.

For example, you might have a 401k plan, a Roth IRA, and a joint brokerage account.

If your ideal asset allocation is 60% stocks and 40% bonds, instead of trying to have each of these investment accounts have this allocation, add up the values of each and go from there.

Let’s say your accounts have the following values:

- 401k Plan: $25,000

- Roth IRA: $15,000

- Joint Account: $10,000

In total you have $50,000 invested.

Make sure that 60% or $30,000 is in stocks and the other 40% or $20,000 is in bonds.

This gives you a lot more freedom to buy and sell in your tax advantaged accounts as well as directing future contributions to get everything balanced.

#5. Strategically Take You Required Minimum Distribution

If you are of retirement age, you can take money out of your retirement plans in a strategic way that gets your back to your original allocation.

For example, if you have a larger percentage in stocks than you are comfortable with, you can take a distribution from your stock holdings only.

This will change your actual allocation closer to your ideal asset allocation, and as a result, bring your level of risk down.

Of course, this isn’t cut and dry, so you should review your financial situation to see if this makes sense for you.

And if you have an investment advisor, you can speak with them about this idea.

#6. Invest In Target Date Funds

If you are just starting out investing, to solve the problem of rebalancing completely, choose to invest in target date funds.

These funds will automatically adjust their asset allocation as the years go by and you get closer to retirement age.

So when you first start investing at age 30, you pick a fund with your target retirement date.

In this example, your allocation might be 80% stocks holdings and 20% bond investments.

But by the time you reach age 60, you might have 40% stocks and 60% bonds.

You did nothing here.

The fund does the rebalancing on its own, over time.

#7. Invest With A Robo-Advisor

Another option for those just starting out is to invest with a robo-advisor.

These online brokers simplify investing by taking care of all the work for you.

You simply answer some questions about your risk tolerance and goals and set up a monthly investment amount.

They will pick the ideal allocation for you, reinvest dividends, and rebalance your portfolio for you.

The best one in my opinion is Betterment.

They are one of the originals and have added new features, keeping them ahead of the pack.

To learn more about Betterment, click the link below.

Frequently Asked Questions

I get asked a lot of questions about rebalancing.

Here are the most common ones.

How often should I rebalance?

A good rebalancing strategy is to rebalance your portfolio once a year.

Anything more than annual rebalancing is overkill.

Keep things simple and pick a time of year and stick with it.

Some people choose June while others select December.

It is completely up to you, just make sure you do it every year at the same time.

At what deviation should I do portfolio rebalancing?

Many investors make the mistake of thinking they need to rebalance the moment one asset class is out of balance.

This isn’t true.

The general rule of thumb is to wait until you have at least a 5% deviation from your preferred target asset allocation.

So if you have a 60% stock portfolio and you have 64% in stocks now, you don’t need to rebalance.

If you were are 72% stocks, then you would want to perform portfolio rebalancing.

Should I look at my investments as one big investment portfolio or individual portfolios?

This is an individual choice.

Some people like looking at each portfolio separately while others like the idea of just having one entire portfolio.

I like looking at my investments as one portfolio as it saves me time.

Can rebalancing my portfolio increase my returns?

This depends.

If you are constantly selling stocks and putting the money into bonds because bonds return less than stocks, then chances are you won’t be increasing your returns.

But if you are selling small cap stocks and putting the money into large cap stocks, then you could see a small boost in your overall return.

With that said, don’t let this stop you from thinking you don’t need to rebalance your portfolio.

If you don’t rebalance, over time you will be taking on a higher level of risk than you are comfortable with.

And at some point, when the market drops, your riskier portfolio is going to cause you to lose a lot more money than you want.

Is there a smart way to have my investment portfolio built?

Yes.

Ideally, you want to keep the majority of bonds or fixed income securities in your tax deferred accounts.

This is because bond funds pay monthly income and this income is taxed at ordinary income rates.

As a beginning investor, this increase in your taxable income won’t be significant.

But as your wealth grows it can be.

By putting these investments in a retirement account, you don’t pay taxes on this income since it grows tax deferred.

Final Thoughts

At the end of the day, there are a handful of ways you can rebalance a portfolio.

Which one is best for you might not be best for someone else.

You need to take the time to review your investment goals and decide which one is best for you.

Just make sure you make it a point to rebalance your investment portfolio.

The last thing you want is to lose a lot more money than you are comfortable with and then overreact by making made investment decisions.