THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

Looking for a smarter way to grow your money without gambling it away?

Whether you’re saving for a down payment, building an emergency fund, or just want your cash to do more than sit in a savings account, you’re not alone.

Many people are asking the same question: Where can I park my cash short term without taking big risks?

The good news?

There are options – low risk investments that offer solid returns without locking up your money for decades.

If you’re looking to grow your money safely over the next 1 to 5 years, these options may work for you.

In this guide, we’ll explore some of the best short term investment options available right now.

Whether you’re just getting started or want to fine-tune your financial plan, this article will give you real, actionable ideas to help you make your money work harder – without the stress.

The 10 Best Short Term Investments For Your Money

| Investment Type | Advantages | Drawbacks |

|---|---|---|

| High Yield Savings Account | -Easy access to funds (highly liquid). -FDIC insured (up to $250,000). | -Interest rates can fluctuate. -Lower returns compared to other investments. |

| Bank CD | -Guaranteed fixed return. -FDIC insured. | -Early withdrawal penalties. -Lower liquidity (locked-in for a term). |

| Broker CD | -Access to higher CD rates through various banks. -Can be sold on the secondary market (more flexible). | -May sell below original value if cashed out early. -Not all brokerage CDs are FDIC insured, depends on the issuing bank. |

| Money Market Accounts | -Higher interest than standard savings accounts. -Check-writing and debit card access (in some cases). | -May require a high minimum balance. -Interest rates not as competitive as some online options. |

| Savings Bonds | -Backed by the U.S. government. -Tax-deferred interest until redeemed. | -Must be held for at least 1 year (not liquid). -Penalty if cashed before 5 years (lose 3 months’ interest). |

| Treasury Bills | -Very low risk (government-backed debt securities). -Highly liquid and easy to sell. | -Lower yields compared to riskier investments. -Interest is subject to federal income tax. |

| Invest in Small Businesses | -Higher rate of return than other options. -Ability to invest spare change. | -Potential to lose money. -Interest rate could drop in the future. |

| Invest in Real Estate | -Higher rate of return than other options. -Can invest with as little as $10. | -Cannot sell for 6 months. -Redemption fee if sold within 5 years. |

| Short Term Bond Funds | -Diversification across multiple bonds -Potential for higher returns than .savings accounts or CDs. | -Not insured, value can fluctuate. -Interest rate risk (value may drop if rates rise). |

| Peer 2 Peer Lending | -Potential for higher returns. -Supports individual borrowers or small businesses. | -Higher default risk (not insured). -Funds may be tied up for the loan term (lower liquidity). |

#1. High Yield Savings Accounts

The safest place to put your money is a traditional savings account at your bank or credit union.

The problem with these accounts is they pay little to no interest.

So while you don’t lose money because the money you put in is safe, you do lose when it comes to purchasing power.

For example, if you are earning 1% on your savings and inflation is 4%, your money is growing slower than prices are rising.

If you have $100 saved, in one year you will have $101. But something that costs $100 today will cost $104 in one year.

As you can see, you didn’t lose your money in your bank account, but you are falling behind when it comes to keeping up with inflation.

The good news is that many banks and credit unions offer high yield saving accounts.

These are the exact same as a normal savings account except that they pay higher interest rates.

Since most banks offer these accounts, you need to find a bank that is not only trustworthy, but also pays a high interest rate.

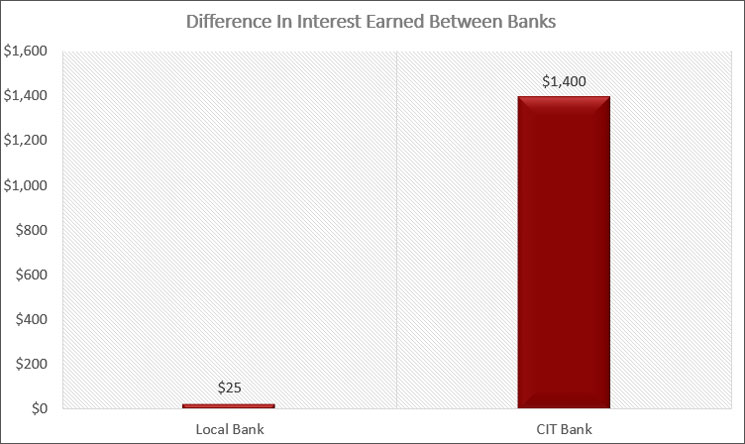

One of my favorite banks is CIT Bank.

With some of the highest paying interest rates in the U.S. CIT Bank stands out as offering the best savings accounts, specifically the Savings Connect Account. Add in ease of use and great customer service, and you have a clear winner.

This bank offers an online savings account with an interest rate that is historically one of the highest in the country, allowing you to earn a lot more interest.

And they consistently rank at the top of the list of highest interest paying accounts all the time.

Current Rate You Can Expect to Earn: Between 4.25% and 5% depending on the bank

#2. Bank Certificates of Deposit

Investing in a certificate of deposit (CD) is a great way to earn a higher interest rate on your money.

The difference with a bank CD is the potential for higher interest, also known as yield.

In return for this higher yield you have to lock your money up for a period of time.

With a savings account, you are free to take your money out of the account whenever you want.

But with a CD, you have a period of time that you have to leave the money in the account.

You know the length of this period of time because you choose the term.

Most common CD terms are 6 months, 1 year, 18 months, 2 years and 5 years.

The longer you lock your money up, the higher the interest rate you will earn.

Of course, if you really need the money, you can still close the CD early and get your money back.

But by doing this, you will typically forfeit 3 months worth of interest payments.

Note that there are some CDs that offer no penalty if you close the CD early, but they pay a slightly lower interest rate because of this.

Finally, there are some CDs that offer the option to increase your interest rate one time during the term.

Since your interest rate is locked when you open the CD, you could lose out if interest rates rise with a typical CD.

By letting you increase your rate one time, you can lower the chances of this risk.

Current Rate You Can Expect to Earn: Between 4% and 4.50% depending on the term

#3. Brokerage Certificates of Deposit

You can also buy a CD through your broker, like Schwab or Fidelity.

Doing this offers two main benefits: higher interest and more liquidity.

Most CDs you can buy through a broker offer a higher interest rate than from a bank.

When I was investing in these CDs a few months ago, a 6-month bank CD was paying 4.5% while a broker CD was paying 5.25%.

The other benefit is that you can sell your CD at any time on the secondary market.

This is a fancy way of saying there are investors always looking for CDs and as a result, you can sell your CD before maturity.

There is no penalty for doing so, but interest rates will determine how much or how little you can sell it for.

Current Rate You Can Expect to Earn: Between 4% and 4.75% depending on the term

#4. Money Market Accounts

Money market accounts, or money market funds, are a way for you to earn higher interest without locking your money up like with a certificate of deposit.

There are 2 types of money market accounts.

The first is virtually the same as a savings account.

The only real differences are that you tend to need a higher balance in the account, for example $25,000 or more and you can write checks on the account.

Banks will pay a higher interest rate on a money market account since you are depositing more money.

The second type of money market account is a money market mutual fund.

These accounts invest in short-term bank instruments and some brokers call them a cash management account because you can deposit money, write checks, and in some cases, have a debit card.

The underlying value of the money market fund stays at $1 (although back in 2008 after the housing collapse, some funds did “break the buck”).

Essentially, with a money market fund, your money is safe and you will earn a little more interest than a basic account at the bank.

Current Rate You Can Expect to Earn: Between 3.60% to 4.50% depending on the bank

#5. Savings Bonds

Savings bonds are another short term investment option.

While typically considered long term investments, you can use these government securities in the short term.

Savings bonds are backed by the full faith and credit of the federal Government and are therefore considered free of default risk.

Currently there are two types of savings bonds available for purchase, the EE Series and Series I.

The difference is how they pay interest.

- EE Series savings bonds pay a fixed rate of interest. The rate you earn is set when you purchase the bond, and remains constant for the life of the bond.

- I Bonds pay fixed rate of interest, plus an adjustable rate. The interest rate on an I Bond is made up of two components, a fixed rate component and a floating rate component. The fixed rate component on an I Bond is set when the bond is purchased and remains constant for the life of the bond. The floating rate component is reset every 6 months and is based on the current level of inflation.

The interest rate on an EE Series savings bonds is lower than what you will find with many of the other options listed here.

But there are some interesting things to consider.

First, if you keep your EE Bond for 20 years the government guarantees that it will at least double in value.

When you do the math, this comes out to a return of 3.5% over the life of the bond.

This works because if you cash in your bond after 20 years and it is not worth double the purchase price, the government will make an adjustment to the final value of the bond so it will be worth double what you paid.

The second interesting thing to consider is that while you will owe federal income tax on the interest you earn on the bond, you will not owe any state income tax.

Finally, you can avoid taxes altogether by using the bonds and the interest to pay for higher education.

The same tax benefits of the EE bonds are true for I bonds as well.

Finally, you can cash in a savings bond at any time after holding the bond for 1 year.

However, if you cash the savings bond in before holding it for 5 years, then you have to give up 3 months worth of interest.

After 5 years you can cash the bond in at any time without penalty.

Also keep in mind that an individual can purchase up to $10,000 worth of EE bonds and $10,000 worth of I bonds in any given year.

Current Rate You Can Expect to Earn: Around 3%

#6. Treasury Bills

Treasury Bills, commonly known as T-Bills, are short term debt securities issued by the U.S. government.

They are considered one of the safest investments available because they are backed by the full faith and credit of the U.S. Treasury.

T-Bills are typically sold in terms ranging from a few days to one year, making them ideal for investors looking for short-term, low-risk opportunities.

T-Bills are purchased at a discount to their face value, and investors earn a return when the bill matures and the full face value is paid.

For example, you might buy a $1,000 T-Bill for $980 and receive the full $1,000 at maturity, with the $20 difference being your earnings, or the “interest” you earn.

Because there are many buyers for these government bonds, they are highly liquid, allowing you sell at any time.

Current Rate You Can Expect to Earn: Between 4% and 4.20% depending on the term

#7. Invest In Small Businesses

Before I told you how you can earn 192% more interest by opening an account with CIT Bank.

Here I will do you one better.

You can earn close to 200% more interest by purchasing Worthy Bonds.

What are Worthy Bonds?

It is an investment that has your investment loaned out to small businesses to fund their inventory needs.

They also help fund real estate projects as well.

Worthy charges a low interest rate to the small business and then Worthy turns around and gives you 7% on your investment.

By investing with Worthy Bonds, you earn 7% on your money.

Looking to safely earn a higher return on your money? Worthy Bonds offers 5% 7% interest on your money. Invest in small businesses and earn a return for doing so. New users get a $10 bonus when purchase your first bond.

The catch is there is some risk to your investment.

In fact, this is the first short term investment that does put your principal at risk.

Understand though that this risk is small.

Worthy is required to have a contingency fund of money in case a small business doesn’t pay back their loan.

In this case, Worthy would use the money in the contingency fund to pay you the 5% on your savings.

In other words, Worthy Bonds has an emergency fund to protect investors.

The odds of this happening however are slim since the company goes to great lengths to loan money out to high quality businesses.

Additionally, the loans are backed by the inventory of the small business.

You can get started with Worthy Bonds with as little as $10. You can even set up your account to invest your spare change.

This works by having Worthy round up your purchases to the nearest dollar and invest your spare change to buy more bonds.

If you average $500 in round ups a year, in 10 years you will have an additional $6,600!

Current Rate You Can Expect to Earn: Currently 7% until January 2026, then 5%

#8. Invest in Real Estate

I’m a big fan of investing money in real estate.

The problem is you need enough money for a down payment to buy a property.

And if you plan to rent it out, there is a lot of work there, unless you hire a management company, and then there is an added cost.

To sidestep this, I’ve been investing with Arrived.

It’s a crowdfunding platform that pools investors money and buys properties.

Then quarterly, I earn a dividend based on my share of ownership.

I also earn a return when the appreciated property is sold.

The reason Arrived is a short term investment option is because of their Private Credit Fund.

Looking for an easy way to get started investing in real estate without a lot of money? Look into Arrived Homes. Pick the single family houses in the parts of the country you want to invest in and earn passive income.

This fund invests in short-term loans to fund real estate projects.

Currently you earn around 8% and invest with as little at $10.

The drawboack of this idea?

It’s not the most liquid investment because you have to keep your money locked up for at least six months before you can sell, and there is a fee if you sell in less than five years.

Current Rate You Can Expect to Earn: Currently 8%

#9. Short Term Bond Funds

The next short term investment to consider is short term bonds.

The main difference with short term bonds over the other ideas mentioned is that this is the first one that you have a higher risk losing principal.

In other words, if you invest $1,000 in short term bonds, you could end up with $900 or less.

As far as the interest rate short term bonds pay, it all depends on overall rates and what the Federal Reserve is doing.

But before you run off to buy short term bonds, you have to understand how they work.

Without confusing you completely, know that when bond prices rise, interest rates fall.

And when bond prices fall, interest rates rise.

For example, take a bond that is selling for $100 and yielding 3%.

If rates rise to 3.25%, the price of the bond will drop below $100. While you lose principal, you do earn more interest.

Understand that I recommend investing in bond funds over individual bonds as it is easier and more cost effective.

The best way to invest in short term bonds is through ETFs and mutual funds.

- Read now: Click here to understand how ETFs and mutual funds differ

- Read now: Learn the basics of mutual funds

By investing in short term bond funds, you buy a basket of bonds at various prices and interest rates, diversifying your risk.

You also buy bonds with various maturity dates.

This is a fancy way of saying when the bond ends and the investor gets their principal investment back.

An ideal portfolio to invest in would consist of the following bonds funds:

- iShares Short Treasury Bond ETF (SHV)

- iShares Ultra Short-Term Bond ETF (ICSH)

- iShares 0-5 Year Investment Grade Bond ETF (SLQD)

By creating this portfolio of interest paying bonds, you would earn an OK yield and has the potential to offer growth of your principal as well.

Current Rate You Can Expect to Earn: Between 5% and 6%

#10. Peer To Peer Lending

Another lower risk option is to looking into peer lending, or p2p lending.

This is where people who need money crowdfund their loan by skipping the bank.

Here is how it works.

Let’s say I need $10,000 for a car.

I go in Lending Club or Prosper and after doing a background check on me, these sites allow my loan to be posted for investment.

You see my loan and the interest rate you will be paid and decide to invest $200.

Assuming others invest enough to hit my $10,000 goal, the loan is made.

Now every month for the next 5 years you will get a portion of your $200 investment back, plus interest.

The interest rate varies by loan and borrower and you can build a portfolio of investments by investing in a handful of loans.

Current Rate You Can Expect to Earn: Between 5% and 9%

Advantages And Drawbacks

Of course with any investment, there are advantages and drawbacks.

This is true with the types of short term investments I list above.

Advantages

- Safe principal. In most cases, you won’t be risking your principal when you invest for the short term.

- Easy to predict. Since your principal is safe and you know the interest rate you will earn, it is easy to do the math to see how much money you will end up with.

- Flexibility. It’s easy to get your money when you need it, and not have it tied up long term.

- Small investment. You can generally start putting money in these financial products with as little as $1.

Drawbacks

- Lower returns. Because the investments tend to be safe, they pay lower returns.

- Taxes. When it comes to bonds, you are paying ordinary income tax rates if you invest in a taxable account.

- Many options. This is a benefit except if too many choices makes it harder for you to decide on one investment.

- Interest Rate Risk. The biggest risk you face when looking to make money over the short term is fluctuating rates. Depending on how rates move, you might earn less money, or with some investment ideas, lose some of you initial investment.

Investments to Avoid

When investing for the short term, there are some investments you want to avoid, mostly because the risk of losing money is too great.

The first is with individual stocks.

While you can earn a high rate of return, there is too much risk of losing money, especially if you need the money in one year or less.

Another investment to avoid is corporate bonds.

Corporate bonds are debt issued by companies and the money they make by selling them is to grow or expand into new business lines or territories.

They tend to pay higher rates of interest compared to government bonds, mainly because of the increased risk of default.

While bonds overall are a low risk investment, corporate bonds are a better option for long term investors.

Short Term Investment Strategies

With all of the types of short term investments listed, you might be confused and a little overwhelmed as to what the best options are for you.

Luckily, I have you covered.

Here is a breakout of short term investment strategies you can use right now to earn more interest without much risk.

By following these strategies, you will know exactly how to invest your money.

#1. Start Off With High Yield Savings Accounts

You need to have a cushion for emergencies and the best place for this money is an account at your bank.

While your needs may differ, I suggest keeping $10,000 in this account.

This allows for quick access to your money should you need it.

I realize saving $10,000 sounds intimidating, but you can do it.

Just break it out into smaller goals, like saving $1,000 at a time and you will get there faster than you think.

Again, I recommend going with CIT Bank since you will be earning a healthy amount of interest on your savings.

Of course, most any online bank will do, as most tend to pay higher rate of interest than a traditional brick and mortar bank or credit union.

Finally, I recommend you have a separate account for each of your savings goals.

This helps to keep you motivated as you can see where you stand with each goal.

#2. Create A CD Ladder

Once you have $10,000 in savings at the bank, you can begin to create a ladder of CDs.

This works by having you invest in certificates of deposit that have different maturity dates and various interest rates.

By doing this you limit the risk of rising rates while your money is locked up.

I suggest you invest your money in 4 CDs with the following maturities:

- 12 Month (1 year) CD: $1,500

- 18 Month (1 ½ year) CD: $1,500

- 24 Month (2 year) CD: $1,500

- 60 Month (5 year) CD: $1,500

In total you are investing $5,500 in bank CDs. When each CD matures, you simply reinvest the money for the same term in a new CD.

#2a. Invest In Worthy Bonds

As an alternative to building a ladder with certificates of deposit, you can invest in Worthy Bonds.

I encourage you to take advantage of their round up feature to help you speed up the process of saving money quickly.

#2b. Invest with Arrived

Another alternative to a CD ladder is Arrived.

You will get a higher rate of return with a relatively safe investment.

But you cannot redeem your money for six months and are charged a small fee is you redeem before five years.

The good news is they have a minimum investment of just $10.

#3. Invest in Short Term Bond Funds

You now have $15,500 invested between savings and bank CDs or Worthy Bonds/Arrived.

Your next step is investing in short term bond funds.

To do this, buy the following bonds:

- iShares Short Treasury Bond ETF: (SHV)

- iShares Ultra Short-Term Bond ETF: (ICSH)

- iShares 0-5 Year Investment Grade Bond ETF: (SLQD)

You want to make sure you have the following percentage of each in your investment portfolio:

- 45% – iShares Short Treasury Bond ETF (SHV)

- 35% – iShares Ultra Short-Term Bond ETF (ICSH)

- 20% – iShares 0-5 Year Investment Grade Bond ETF (SLQD)

This will diversify your money and provide you with a nice monthly income stream.

The downside to this is every month your monthly income is getting taxed at ordinary income rates, which is higher than investment taxes.

So before you do this, review your financial situation to make sure it makes sense for you.

Frequently Asked Questions

There is a lot of confusion and some mystery surrounding the many types of short term investments.

I created this FAQ section to help you understand exactly what you are getting into when investing in these investment types.

When should I invest in short term investments?

When it comes to investing, your time horizon plays a huge role into what you actually invest in.

Without taking into account your time frame, you could end up investing in an asset that is too risky or one that carries too little risk and therefore won’t provide the return you need.

Therefore, you need to make sure you pick the right investment based on when you need the money, your financial goals, and risk tolerance.

Below is a chart for your reference.

| When Money is Needed | Best Investment |

|---|---|

| Less Than 1 Year | Cash (Savings Account, CD) |

| Between 1-5 Years | Cash & Short Term Bonds |

| More Than 5 Years | Stocks & Bonds |

From the chart you can see that if you have a short time horizon, such as needing your money in less than 5 years, then you should be investing in cash and/or bonds.

Investing in traditional long term investments like stocks or equities at this point is not advised since you would risk losing your principal in return for a higher rate of return.

This risk is simply too great and you should stick with cash and/or bonds.

Are short term investments safe?

The next question I get asked about the different types of short term investments is are they safe.

For the most part, they are safe.

Of course, if you listen to talk radio, there will be ads touting all sorts of safe investments, many of which are nowhere near safe and others even I haven’t heard of.

Aside from these outliers, short term investments are safe to invest in.

Is my principal is safe?

The overwhelming majority of times when investing in checking, savings, and certificates of deposits, the principal you invest is safe 99.99% of the time.

The only way you will lose your principal is if the bank where the investment is held at goes under and it wasn’t covered by FDIC insurance.

Additionally, if you had more invested than the Federal Deposit Insurance Corporation coverage amount allows, your extra savings could be at risk.

When do I risk losing money?

Even though these are safe investments in the sense you will never lose principal, depending on the interest rate you are earning, you still risk losing money to inflation.

I’ve talked before about inflation, but too many investors ignore it.

Over time, inflation eats away at the purchasing power of your money.

We see this all the time.

I remember as a kid a pack of gum costing me $0.50. Now it costs $1.99.

This is the effect inflation has on prices. It causes prices to rise over time.

Historically, inflation runs between 2-3% annually.

If your savings account earns you 1% per year, you are losing out to inflation.

Let’s look at the numbers to see this in action.

Let’s say you have $1,000 and want to use it buy a home theater system that also costs $1,000.

But you don’t want to buy it now, you want to buy it in 1 year after you have your new house.

You decide to invest your money in a savings account earning 1% annually.

During this time, inflation is running at 3% annually.

After one year, you earned $10 in interest, making your savings worth $1,010.

Because of inflation, the home theater system that cost $1,000 at the beginning of the year now costs $1,030 at the end of the year.

Your savings account a safe type of investment because you didn’t lose your original $1,000. But it is not a safe investment because inflation is outpacing your return.

While you earned $10 in interest, the cost of the home theater system rose by $30, thus you “lost” $20.

This is the danger of safe types of investments.

You sleep at night because you are not losing the money you saved or invested.

But you are losing purchasing power and as a result, need to save more money every year.

This is why they call inflation the silent killer. It slowly destroys your finances behind the scenes.

The good news is that by earning an interest rate in the 2-3% range, you keep pace with inflation and it doesn’t have a negative impact on your wealth.

Are there any other risks with investing for the short term?

The only other risk factors is interest rate risk.

Because rates can change, you risk not earning enough money to meet your goal.

This is why it is critical to invest your money in different types of short term securities to limit this risk.

What are high yielding safe short term investments?

Unfortunately, there is no such thing as a high yielding short term investment, regardless of what the man on the radio or late night television is trying to sell you.

Always remember that risk and return are related.

The higher the risk, the higher the potential return you can expect. The lower the risk, the lower the potential return you can expect.

As of now, the highest yield you can expect to earn and still have your money safe in terms of not losing money is with Worthy Bonds or CIT Bank.

In my opinion, they are the best short term investments you can make and this is where I put my money.

Where is the best place to invest my money for 1 year?

If you need your savings within 1 year, the best short term investing options are an online savings account or a bank or broker CD.

The ultimate answer will be the interest rate.

I pick these options because the risk of losing money is extremely low and you money is FDIC insured.

I would first consider an online bank since they are easy to open and you withdraw your money at any time without penalty.

Pick a few and see which one offers the best rates.

From there, I would look at a few different banks for their rate on a 1 year CD.

If the rate is higher than with a savings account, invest in the CD.

If the rate is lower, then put your money into an account with CIT Bank.

Is a Roth IRA a good short term investment?

A Roth IRA is a good place for a short term investment since you can withdraw your contributions without any tax consequences or penalties.

You just have to make certain you only are taking out as much as you invested.

This is because while earnings are tax free if you are over 59 ½ they are subject to taxes and penalties if you withdraw them before you turn 59 ½.

Also, be sure to only invest in less risky investments.

This means no stocks if you expect to need the money in less than 5 years.

Should I invest in stocks in the short term to earn a higher return?

While stocks do tend to offer a higher return than many of the investments on this list, the risk is that you can lose money.

And since you need the money over the short term, this risk is not worth it.

However, if you insist on stock trading to try to make money in a short amount of time, there are some things you should know, the most important being your trading system.

A lagging system can cost you trades, especially during high-volume moments.

A high-performance trading computer is designed to handle heavy workloads like streaming data, multi-monitor setups, and fast platform switching.

These machines are built with the specific needs of traders in mind—prioritizing speed, uptime, and responsiveness.

It’s a reliable foundation for anyone serious about day trading.

With a ninjatrader vps, you don’t have to worry about your trading platform crashing or disconnecting at a crucial moment.

TraderVPS provides always-on servers optimized for NinjaTrader, ensuring stable performance and ultra-low latency.

This setup is ideal for traders using custom indicators, automated strategies, or managing fast-moving markets.

It brings peace of mind by keeping your trades online and responsive at all times.

Final Thoughts

Overall, when it comes to the types of short term investments, you have a handful of choices.

Just pick the right investment vehicles for you goals and you should be all set.

Remember not to fall victim of taking on more risk just for a higher return if you need the money in less than 5 years.

Trust me, the risk is not worth it.

Accept that you are earning less interest and be done with it.

As you saw from the many options I listed, you can still earn a decent return without taking on the added risk.

Jon,

Great overview – I especially like how you recap things and remind folks not to chase yield if their time horizon is less than five years. So many folks get this wrong and end up creating major problems for themselves.

I try to keep as little as possible in these short-term investments because of the poor interest rate they give me. Instead I put spare cash I don’t need into long-term investments like dividend stocks, especially those yielding above 5%.

From all of these, I think I prefer bond investment. Yes, there’s a possibility of losing your principal, but just like you said, as long as you keep it until it matures, it would be the best option.

I have some of my emergency fund money in bonds. Most is in cash, but I take the “excess” and put it into bonds for a higher return.