THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

When you first hear about the Trump Account, it’s easy to dismiss it as just another government program, or even tune it out because of the name.

That would be a mistake.

Politics aside, this new investment account could become one of the most powerful wealth-building tools available for children.

Imagine giving a newborn a small investment that has nearly two decades to grow before they can touch it.

Then imagine that, at age 18, when many young adults have little or no taxable income, they may have an opportunity to convert those savings into a Roth IRA, allowing decades of future investment growth to potentially become tax free.

Used strategically, that single decision could be worth tens or even hundreds of thousands of dollars over a lifetime, depending on how much the account grows and future tax rules.

Of course, Trump Accounts aren’t perfect.

They come with contribution limits, withdrawal rules, and restrictions that make them very different from a Roth IRA, a 529 college savings plan, or a UGMA/UTMA account.

In this guide, you’ll learn exactly how Trump Accounts work, who qualifies, how the money is invested, what happens when your child turns 18, and why many financial experts believe the biggest opportunity isn’t the $1,000 government contribution.

We’ll also compare Trump Accounts to other popular savings options so you can decide whether they deserve a place in your family’s financial plan.

What Is a Trump Account?

A Trump Account is a long-term investment account created for children under the One Big Beautiful Bill tax legislation signed into law in 2026.

Trump Accounts give eligible newborns a $1,000 government-funded investment to help jump-start their financial future, and parents, grandparents, and others can contribute additional money each year.

Think of it as planting a tree for your child on the day they’re born.

The sooner it’s planted, the more time it has to grow.

Over the next 18 years, the money can potentially grow through investments, and once your child becomes an adult, they may have several options for using the account.

This includes a strategy that could allow decades of future investment growth to become tax free.

Unlike a savings account that earns a small amount of interest, a Trump Account is designed to be invested in the stock market.

While investments can go up and down over short periods, history has shown that long-term investing has generally rewarded patient investors.

The biggest takeaway is this: the $1,000 government contribution is nice, but the real value comes from giving your child’s investments as much time as possible to grow.

How Does a Trump Account Work?

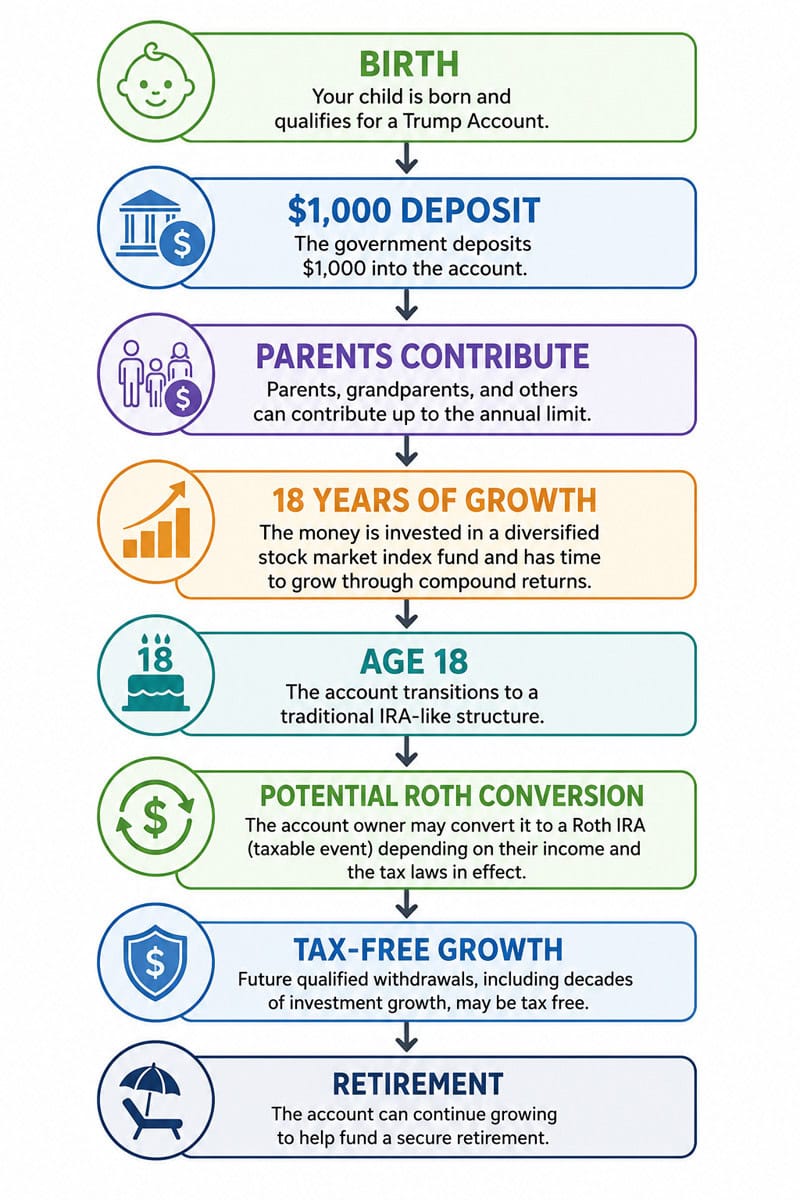

The easiest way to understand a Trump Account is to follow it from birth through adulthood.

Step 1: Your Child Receives the Account

If your child qualifies under the program rules, the federal government contributes $1,000 to open the account.

To qualify for the $1,000 they must be born between 2026-2028.

However, any child under 18 years old can open the account.

They just won’t be eligible for the $1,000.

But, Michael Dell, the founder of Dell Computers, made a charitable donation of $6.25 billion.

This means the first 25 million American children age 10 and under living in ZIP codes with median incomes below $150,000 will receive an additional $250.

Step 2: Family Members can Add Money

Parents, grandparents, relatives, and even family friends can contribute additional money, up to the annual contribution limit established by law.

Instead of buying another toy for every birthday, imagine grandparents contributing $100 each year.

Those small gifts could potentially grow into thousands of dollars by the time your child becomes an adult.

The maximum annual contribution is $5,000.

Step 3: The Money is Invested

The funds aren’t meant to sit in cash.

They’re invested in a diversified stock market index fund, allowing the account to benefit from long-term market growth.

While no investment is guaranteed, history has shown that the longer money stays invested, the greater its potential to grow through the power of compound returns.

Step 4: The Account Grows Over Time

For the next 18 years, contributions and investment earnings remain in the account.

You don’t have to constantly monitor it or make complicated investment decisions.

In many ways, it’s designed to be a “set it and forget it” investment for your child’s future.

Step 5: Everything Changes at Age 18

This is the part most articles barely mention, but it’s arguably the most valuable feature of the entire program.

Once your child turns 18, the account is generally treated much like a traditional IRA.

That opens the door to a potential Roth IRA conversion strategy that could dramatically reduce, or even eliminate, taxes on decades of future investment growth.

We’ll cover exactly how that works later because it may be the single biggest reason parents choose to fund a Trump Account beyond the initial $1,000.

At a Glance: How a Trump Account Works

| Age | What Happens |

|---|---|

| Birth | Eligible child receives a $1,000 government contribution. |

| Childhood | Parents, grandparents, and others can contribute additional money (subject to annual limits). |

| Birth to 18 | The money remains invested and has the opportunity to grow through compound returns. |

| Age 18 | The account transitions to a traditional IRA-like structure, creating the potential for a Roth IRA conversion strategy. |

| Adulthood | The account can continue growing for retirement or be used according to the program’s rules. |

Why Parents Are Paying Attention to Trump Accounts

The biggest advantage of a Trump Account isn’t the $1,000 government contribution, although that’s certainly a nice bonus.

It’s the amount of time the money has to grow.

Most people don’t begin investing until they’re in their 20s or 30s.

Many don’t even start until later than that.

A Trump Account gives a child an 18-year head start before they even become an adult.

That’s important because the earlier you invest, the more powerful compound growth becomes.

Imagine rolling a snowball down a hill.

At first, it barely grows.

But as it keeps rolling, it picks up more snow, gets bigger, and begins growing faster and faster.

Investing works much the same way.

Your investment earns returns.

Then those returns begin earning returns of their own. Over time, that compounding effect can become incredibly powerful.

That’s why even relatively small contributions made consistently over many years can grow into surprisingly large balances.

The other reason many financial planners are excited about Trump Accounts is what happens when the child turns 18.

Because many young adults have little or no taxable income, they may have an opportunity to convert the account to a Roth IRA while paying little or no federal income tax on the conversion.

If done strategically, decades of future investment growth could potentially be withdrawn tax free during retirement.

We’ll explain exactly how that strategy works later in this guide.

Who Should Consider Opening a Trump Account?

A Trump Account won’t be the right choice for every family.

However, it may be worth considering if you:

- Have a newborn or young child and want to start investing early.

- Want family members like grandparents to help build your child’s future.

- Are already saving for your child’s long-term financial goals.

- Want another tax-advantaged account in addition to a 529 plan or custodial account.

- Like the idea of giving your child a financial head start before adulthood.

On the other hand, if your primary goal is paying for college, a 529 plan may still be a better fit.

Likewise, if your child already has earned income from a part-time job, a custodial Roth IRA offers benefits that a Trump Account can’t match.

The good news is that these accounts don’t necessarily compete with one another.

Many families may find that using multiple account types together provides the greatest flexibility.

How Much Could a Trump Account Be Worth?

Here’s where things get exciting.

Many people hear about the $1,000 government contribution and assume that’s all there is to it.

In reality, the account’s long-term value depends far more on how much is contributed over time and how long the money remains invested than on the initial deposit.

To put that into perspective, let’s look at a few hypothetical examples.

We’ll assume:

- The account earns an average annual return of 8% (actual returns will vary).

- Contributions are made at the end of each year.

- The money remains invested until age 18.

In the next section, we’ll see how different contribution amounts can dramatically change the account’s value, and why even an extra $25 or $50 per month can make a meaningful difference over time.

How Much Could a Trump Account Grow?

The value of a Trump Account depends on how much is contributed and how long the money stays invested.

The examples below assume:

- A $1,000 government contribution at birth

- Contributions made monthly

- An 8% average annual investment return

- No withdrawals before age 18

- After age 18, the money remains invested without any additional contributions

| Monthly Contribution | Estimated Value at 18 | Estimated Value at 30 | Estimated Value at 65 |

|---|---|---|---|

| Government $1,000 only | $4,000 | $10,100 | $148,800 |

| $25/month | $15,600 | $39,400 | $582,200 |

| $50/month | $27,300 | $68,700 | $1.02 million |

| $100/month | $50,600 | $127,300 | $1.88 million |

| $250/month | $120,400 | $303,200 | $4.48 million |

Note: These examples assume an average annual return of 8%, which is not guaranteed. Actual investment returns will vary, and account values can be higher or lower depending on market performance.

A point worth emphasizing

This table illustrates one of the biggest lessons in investing: time is often more powerful than the amount you invest.

For example, contributing just $50 a month (about the cost of one family dinner out) could potentially grow to more than $1 million by age 65 if the money remains invested.

The initial $1,000 government deposit is a nice head start, but the real wealth comes from making regular contributions, allowing compound growth to work for decades, and avoiding the temptation to withdraw the money early.

Why Age 18 Could Be the Biggest Opportunity

The most talked-about feature of a Trump Account is the $1,000 government contribution.

Ironically, that may end up being one of its least valuable benefits.

The real opportunity comes when your child turns 18 years old.

At that point, the account is generally treated much like a traditional IRA.

That means the account owner may have the option to convert it to a Roth IRA by paying income tax on the converted amount.

At first, paying taxes might sound like a bad idea.

In reality, it could be one of the smartest financial decisions your child ever makes.

The reason comes down to one simple fact: Most 18-year-olds have very little taxable income.

Many are still in high school, starting college, or working part-time jobs.

Because their income is often much lower than it will be later in life, they may qualify for one of the lowest federal income tax brackets they’ll ever see.

That creates a unique window of opportunity.

Instead of waiting until they’re in their 30s or 40s and earning a much higher salary, they may be able to pay taxes on the account while their tax bill is relatively small.

Once the money is inside a Roth IRA, future qualified withdrawals, including decades of investment growth, can generally be taken tax free.

Of course, whether converting the entire account at once is the best strategy depends on the child’s income, tax situation, and the tax laws in effect at the time.

That’s why it’s important to evaluate the numbers before making a decision.

A Simple Example

Let’s see how this might work.

Imagine Emma turns 18 with $50,000 in her Trump Account.

She plans to attend college and works a part-time job that earns $8,000 during the year.

Because her taxable income is relatively low, converting some or all of the account to a Roth IRA could result in a much smaller tax bill than if she waited until she had a full-time career.

Now imagine she leaves that money invested until age 65.

If her investments average an 8% annual return, that $50,000 could potentially grow to nearly $1.9 million.

If the conversion was completed under the Roth IRA rules and all requirements were met, that future growth could potentially be withdrawn tax free.

Here’s what makes this example so remarkable.

Emma never contributed another dollar to this account after turning 18.

She simply left the money invested and allowed compound growth to do the heavy lifting.

By retirement, that original $50,000 had the potential to grow to nearly $1.9 million, all without adding another penny to the account.

Think about how that could change her financial future.

Instead of worrying about whether she’s saving enough for retirement, Emma already has a substantial nest egg working for her before she’s even started her career.

Every dollar she saves in her 20s, 30s, and beyond could become additional retirement savings instead of trying to catch up.

She has more flexibility to buy a home, start a business, raise a family, change careers, or even retire earlier because she began investing decades before most people ever do.

That’s the true power of time.

The government’s initial contribution may have opened the door, but allowing those investments to grow for decades is what has the potential to create life-changing wealth.

That’s why many financial professionals believe the conversion, not the initial $1,000 deposit, may ultimately become the most valuable feature of the entire program.

Why Converting Earlier Can Save Thousands in Taxes

Think about two different people.

Emma converts at age 18.

- Income: $8,000

- Trump Account: $50,000

- Pays taxes while her income is very low.

- Future growth has decades to compound inside a Roth IRA.

Alex waits until age 35.

- Income: $95,000

- Trump Account: $120,000

- Much higher tax bracket.

- Larger tax bill on the conversion.

- Fewer years of tax-free growth remaining.

Neither strategy is automatically right or wrong.

But this example highlights why many families are already talking about the age 18 conversion strategy.

Paying taxes when your income is low can sometimes be much cheaper than paying them later when you’re earning substantially more.

Important Things to Know Before Converting

Before converting a Trump Account to a Roth IRA, keep these points in mind:

- A Roth conversion is generally a taxable event.

- The amount you convert is added to your taxable income for the year.

- Converting too much at once could push you into a higher tax bracket.

- Some people may benefit from spreading conversions over multiple years rather than converting everything at once.

- Tax laws can change, so it’s important to understand the rules that apply when your child reaches age 18.

Because every family’s situation is different, it’s often worth speaking with a qualified tax professional before deciding how much to convert.

Should You Convert All at Once or Over Several Years?

We could compare scenarios like:

| Strategy | Pros | Cons |

|---|---|---|

| Convert everything at 18 | Maximizes tax-free growth; may take advantage of very low income | Could create a larger tax bill in one year |

| Convert over 4 years (18–21) | Helps manage tax brackets; spreads out the tax cost | Less money starts compounding tax-free immediately |

| Wait until after college | May still have low income | Risk of entering a higher tax bracket if income rises quickly |

Trump Account vs. Roth IRA

At first glance, a Trump Account and a Roth IRA might seem similar because both are designed to help build long-term wealth.

However, they serve different purposes and have different rules.

The biggest difference is who can open the account and when.

A child can receive a Trump Account at birth (if they qualify), giving their investments up to 18 extra years to grow before they become an adult.

A Roth IRA, on the other hand, requires earned income.

In other words, your child must have income from a job or self-employment before they can contribute.

That’s why many financial planners don’t view these accounts as competitors.

Instead, they can complement one another at different stages of life.

| Feature | Trump Account | Roth IRA |

|---|---|---|

| Who can open one? | Eligible newborns and children | Anyone with earned income who meets IRS rules |

| Government contribution | Yes, for eligible children | No |

| Parents can contribute | Yes, subject to annual limits | No, unless the child has earned income and contributions don’t exceed that income |

| Investment growth | Tax deferred | Tax free (if qualified withdrawal rules are met) |

| Age requirement | Starts at birth | Requires earned income |

| Best For | Giving children an investing head start | Long-term retirement savings |

Which One Is Better?

If your child has earned income, a Roth IRA is still one of the best retirement accounts available because qualified withdrawals are tax free.

But newborns and young children don’t have jobs.

That’s where a Trump Account fills an important gap.

Instead of waiting until your child gets their first summer job at 16 or 17, they can begin investing from birth.

Those extra years of compound growth could make a tremendous difference over the long term.

In fact, one possible strategy is to use both accounts.

A child could benefit from a Trump Account while they’re young and then begin contributing to a Roth IRA once they start earning income.

- Read now: Discover the pros and cons of Roth IRAs

If the Trump Account is eventually converted to a Roth IRA at age 18, they could end up with decades of tax-free growth and continue adding to that Roth throughout their working years.

The key takeaway is this: you don’t have to choose one or the other.

Depending on your child’s situation, these accounts can work together to build long-term wealth.

Trump Account vs. 529 Plan

If your goal is saving for your child’s future, you’ve probably heard of a 529 plan.

Like a Trump Account, it’s designed to help families invest over many years.

But while these accounts have some similarities, they’re built for very different purposes.

A 529 plan is primarily a college savings account.

It offers valuable tax advantages when the money is used for qualified education expenses, such as tuition, books, fees, and certain housing costs.

A Trump Account, on the other hand, is focused on long-term wealth building.

While there are rules governing when and how the money can be used, many families are most excited about the possibility of converting the account to a Roth IRA at age 18 and allowing the investments to continue growing tax free for retirement.

In simple terms:

- A 529 plan helps pay for college.

- A Trump Account may help build lifelong wealth.

Neither account is automatically better. It depends entirely on your family’s goals.

| Feature | Feature | 529 Plan |

|---|---|---|

| Primary Purpose | Long-term investing and wealth building | Saving for education |

| Government Contribution | Yes, for eligible children | No |

| Tax Benefits | Tax-deferred growth with potential Roth conversion strategy | Tax-free growth when used for qualified education expenses |

| Best For | Retirement and long-term investing | College and education costs |

| Investment Options | Limited by program rules | Wide variety of investment portfolios |

| Can Parents Contribute? | Yes | Yes |

Which One Should Parents Choose?

If paying for college is your highest priority, a 529 plan is still difficult to beat because qualified withdrawals are generally tax free.

However, if your goal is giving your child the greatest possible head start toward financial independence, a Trump Account deserves serious consideration.

Many families may discover they don’t need to choose between the two.

A 529 plan can help pay for college, while a Trump Account can help fund retirement decades later.

Together, they create a balanced strategy that prepares your child for both major milestones.

Trump Account vs. UGMA and UTMA Accounts

A UGMA or UTMA account is another popular way parents and grandparents invest for children.

Unlike a Trump Account or a 529 plan, these are custodial accounts, meaning an adult manages the money until the child reaches the age of majority in their state.

The biggest advantage of a UGMA or UTMA account is flexibility.

The money can generally be used for almost any purpose that benefits the child.

That could include education expenses, buying a car, starting a business, or making a down payment on a first home.

The tradeoff is that there are fewer tax advantages than with retirement-focused accounts.

Another important difference is ownership.

Once your child reaches the age specified under your state’s laws, the money legally becomes theirs.

They can generally spend it however they choose—even if you had something else in mind.

With a Trump Account, the money remains focused on long-term financial goals under the program’s rules.

| Feature | Trump Account | UGMA/UTMA |

|---|---|---|

| Primary Purpose | Long-term investing | General savings and investing |

| Government Contribution | Yes, for eligible children | No |

| Tax Advantages | Tax-deferred growth with potential Roth conversion strategy | Limited tax advantages |

| Investment Flexibility | Limited by program rules | Broad investment choices |

| Use of Funds | Subject to program rules | Nearly any expense that benefits the child |

| Who Controls the Money? | Account owner under program rules | Child gains full control at the age of majority |

Which Account Is Better?

If flexibility is your top priority, a UGMA or UTMA account may be a better fit.

If your goal is helping your child build long-term wealth and potentially retire with a substantial nest egg, a Trump Account may offer greater advantages because of its tax treatment and the possibility of a Roth IRA conversion at age 18.

One thing many parents overlook is that flexibility isn’t always an advantage.

Some families actually prefer having restrictions in place if it encourages their child to leave the money invested rather than spending it shortly after becoming an adult.

Which Account Should You Choose?

There isn’t a single “best” account for every family.

Instead, choose the account that best matches your goal.

| If your goal is… | Consider… |

|---|---|

| Paying for college | 529 Plan |

| Helping a child build retirement savings from birth | Trump Account |

| Investing for a child who already has earned income | Roth IRA |

| Maximum flexibility for future expenses | UGMA/UTMA |

| Building the strongest long-term plan | A combination of multiple accounts |

For many families, the answer isn’t choosing one account over another—it’s using each account for what it does best.

For example, grandparents might contribute to a Trump Account to help build long-term wealth, parents might save in a 529 plan for future education costs, and once the child gets their first job, they could begin contributing to a Roth IRA.

That combination gives the child a strong financial foundation for college, retirement, and everything in between.

5 Common Trump Account Mistakes Parents Should Avoid

A Trump Account has the potential to become a valuable financial tool, but simply opening one isn’t enough.

The decisions you make over the next 18 years can have a much bigger impact than the initial $1,000 government contribution.

Here are five common mistakes to avoid.

1. Thinking the $1,000 Government Contribution Is Enough

Receiving $1,000 from the government is a great start, but it’s unlikely to grow into life-changing wealth on its own.

The real power of a Trump Account comes from making additional contributions whenever possible.

Even small amounts, such as $25 or $50 a month, can add up significantly thanks to compound growth.

If grandparents ask what your child wants for birthdays or holidays, consider suggesting a contribution to their Trump Account instead of another toy they’ll outgrow in a few months.

2. Waiting Too Long to Start Contributing

Time is one of the biggest advantages this account offers.

Every year you delay making contributions is one less year your money has to grow.

Think of compound growth like planting a tree. The best time to plant it was years ago. The second-best time is today.

Even if you can’t afford large contributions, starting small is often better than waiting until you can invest more.

3. Forgetting About the Age 18 Roth Conversion Opportunity

Many articles focus almost entirely on the government’s initial contribution.

In reality, one of the most valuable features of the account may come 18 years later.

Depending on the tax laws in effect and your child’s income, converting the account to a Roth IRA while they’re in a low tax bracket could allow decades of future investment growth to be withdrawn tax free.

That doesn’t mean converting the entire balance at once is always the right move, but it’s a strategy worth evaluating rather than overlooking.

4. Ignoring the Tax Impact of a Conversion

While converting to a Roth IRA can be a powerful strategy, it’s important to remember that Roth conversions are generally taxable.

Converting a very large balance in a single year could increase your child’s taxable income and potentially push them into a higher tax bracket.

In some situations, it may make more sense to convert the account over multiple years instead of all at once.

The right approach depends on the account balance, your child’s income, and the tax rules in place at the time.

5. Assuming This Should Be Your Only Savings Account

A Trump Account can be an excellent addition to your family’s financial plan, but it doesn’t have to replace every other savings account.

Each account serves a different purpose.

- A 529 plan is designed primarily for education expenses.

- A Roth IRA is ideal once your child has earned income.

- A UGMA or UTMA account offers flexibility for a wide range of future expenses.

- A Trump Account is designed to give children a long-term investing head start.

Many families may benefit from using more than one account instead of trying to find a single solution that does everything.

Frequently Asked Questions About Trump Accounts

What is a Trump Account?

A Trump Account is a long-term investment account created for eligible children under legislation signed into law in 2026.

The federal government contributes $1,000 to qualifying accounts, and parents, grandparents, and others can make additional contributions each year.

The money is invested with the goal of growing over time and helping build long-term financial security.

Who qualifies for a Trump Account?

Generally, children born after the program’s effective date who meet the eligibility requirements established by law can receive a Trump Account.

Because eligibility rules can change, it’s important to review the most current IRS guidance or speak with your financial institution before opening an account.

How much money can you contribute to a Trump Account?

In addition to the government’s initial contribution, family members and others may contribute up to the annual limit established under the law.

These limits may change over time, so check the current IRS rules before making contributions.

Can grandparents contribute to a Trump Account?

Yes. Grandparents, relatives, and even family friends may be able to contribute to a child’s Trump Account, subject to the program’s annual contribution limits.

This makes birthdays, holidays, and other special occasions a great opportunity to give a gift that could continue growing for decades.

How is the money invested?

Trump Accounts are designed to invest in a diversified stock market index fund rather than keeping the money in cash.

While investments can lose value in the short term, history has shown that long-term investing has generally produced higher returns than traditional savings accounts.

What happens when my child turns 18?

One of the most important features of a Trump Account occurs at age 18.

At that point, the account is generally treated much like a traditional IRA. Depending on your child’s income, tax situation, and the laws in effect at the time, they may have the opportunity to convert some or all of the account to a Roth IRA.

While the conversion is generally taxable, future qualified withdrawals from the Roth IRA could be completely tax free.

Should my child convert the entire account to a Roth IRA at age 18?

Not necessarily.

Converting the entire balance immediately may be the right strategy for some families, but not for others.

Because Roth conversions are generally taxable, a large conversion could move your child into a higher tax bracket.

Some families may benefit from converting the entire account while the child has very little income, while others may prefer spreading the conversion over several years.

The best approach depends on the account balance, your child’s income, and the tax laws in effect at the time.

Is a Trump Account better than a 529 plan?

It depends on your goals.

If your primary objective is paying for college, a 529 plan generally offers the greatest tax benefits for qualified education expenses.

If your goal is giving your child a long-term investment that could potentially grow for retirement, a Trump Account may be the better choice.

Many families may decide to use both accounts as part of a broader financial plan.

Is a Trump Account better than a Roth IRA?

These accounts are designed for different situations.

A Roth IRA requires earned income, so most young children aren’t eligible to contribute.

A Trump Account allows investing to begin much earlier in life.

Once the child has earned income, they may also begin contributing to a Roth IRA, and at age 18 they may even have the opportunity to convert the Trump Account to a Roth IRA.

For many families, the best strategy isn’t choosing one over the other.

It’s using both when appropriate.

Can a Trump Account lose money?

Yes.

Because the account is invested in the stock market, its value can rise and fall over time.

Short-term losses are possible, especially during market downturns.

However, the account is designed for long-term investing.

Historically, broad stock market index funds have generally rewarded investors who remained invested for many years.

What happens if my child doesn’t go to college?

Unlike a 529 plan, a Trump Account isn’t primarily designed for education savings.

Whether your child attends college, enters the workforce, starts a business, or joins the military, the account continues to exist under the program’s rules.

Many families are most interested in using it as a long-term retirement and wealth-building tool rather than a college savings account.

Are Trump Accounts worth it?

For many families, the answer may be yes.

The $1,000 government contribution provides an immediate head start, but the biggest advantage is the opportunity to begin investing from birth.

Combined with regular contributions, decades of compound growth, and a carefully planned Roth IRA conversion strategy at age 18, a Trump Account has the potential to become a meaningful part of your child’s long-term financial future.

The key isn’t the size of the initial deposit.

It’s giving your child’s money as much time as possible to grow.

Final Thoughts

Whether you love the name or hate it, the reality is that a Trump Account is simply another financial tool. And like any financial tool, its value depends on how you use it.

The $1,000 government contribution is a nice head start, but it isn’t what has the potential to change your child’s financial future.

The real opportunity comes from starting early, contributing consistently, allowing compound growth to work for decades, and carefully planning what happens when your child turns 18.

For many families, the age-18 Roth IRA conversion strategy may prove to be the most valuable feature of the entire program.

If your child can convert the account while they’re in a low tax bracket, decades of future investment growth could potentially be withdrawn tax free, a benefit that could be worth far more than the government’s initial contribution.

Of course, a Trump Account isn’t a replacement for every other savings account.

Depending on your family’s goals, it may work best alongside a 529 plan, a Roth IRA, or other investment accounts.

The key is understanding what each account is designed to do and using the right tool for the right job.

At the end of the day, the biggest lesson has nothing to do with politics or even this specific account.

The earlier you start investing, the more time your money has to grow.

Whether it’s $25 a month, birthday gifts from grandparents, or larger annual contributions, every dollar invested today has the potential to become many more dollars decades from now.

Your child won’t remember every toy they received growing up. But one day, they may be incredibly grateful that you gave them something even more valuable…a financial head start that lasts a lifetime.