THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

Do you ever calculate your net worth?

If you are like many others, the answer is probably no.

But this simple formula can change your finances forever.

In this post I’ll show you how simple it is to calculate your net worth so you can get a clear picture of your financial situation.

I’ll also show you how to understand the answer so you can change your money habits for the positive and reach your financial goals.

So if you finally want to take control of your money, learn how to figure out your net worth below and start seeing changes right away!

How To Calculate Net Worth

What Is Net Worth?

In the simplest terms, your net worth is your current situation financially.

The calculation is straight forward as you take your assets and subtract your liabilities, to come up with a number.

The number you end up with is your net worth.

Here is the simple formula:

Assets – Liabilities = Net Worth

So how do you calculate net worth?

There are 3 simple steps.

Step #1: Calculate Your Assets

The first step in calculating net worth is to gather up all of your assets.

Personally, I break up my assets into four categories:

- Cash: checking and savings accounts, CD’s, physical cash, etc.

- Investment Accounts: stocks, bonds, mutual funds, ETFs, etc.

- Retirement Accounts: IRA’s, 401k, 403b, etc.

- Property: cars, jewelry, household items, house, etc.

You can break these down by account to make things easier to track over time.

For example, if you just have one section called bank accounts, it will be hard to see why the money in this account dropped.

But if you break out checking accounts and savings accounts, you will see the bank account balances in your savings account dropped, helping you to remember you had an emergency you needed to pay for.

The only hiccup for many is when it comes to tangible assets, like real estate and your cars.

When reporting property, be sure to use the market value and not the price you paid for it.

If your car is worth $15,000 and you bought it for $30,000 list $15,000 as its value.

The same idea applies for your house.

List what it is currently valued at, not what you bought it for, and ignore your mortgage balance for now.

In fact, do not take into account any loans here.

If you owe $5,000 on the car, you ignore that for this step.

Simply enter the value of the item if you were to sell it today.

We will tackle the loan in the next step.

Step #2: Calculate Your Liabilities

The next step in calculating your net worth is to gather up all of your liabilities.

Here you will list all of your outstanding debts.

This includes current debt balances for your auto loan, mortgages, student loan debt, credit card debt, etc.

As with the assets section above, I break these out as well.

I like to see the financial progress I am making with paying off these debts.

If you want to create categories for your liabilities, you could use the following:

- Credit Cards: list your credit card balance

- Loans: list all of your loans like mortgage, car loan, mortgage, personal loans, etc.

You would put all of your credit card balances under the credit card category and any loans you have under the loans category.

To be clear, just list the balances you owe in this section.

Look at your most recent statement and record whatever the balance you owe for each.

Step #3: Adding It All Up

Once you have both your assets and liabilities listed, you have to total up each section.

Look at your assets and add all of them up and write down the total.

Now do the same for your liabilities.

I create a section at the bottom for total assets and total liabilities so I can see the complete amounts.

Once you have the totals for each, simply subtract liabilities from assets to get your net worth and see your financial life on one sheet of paper.

For example, if you have $100,000 in assets and $50,000 in liabilities, then your net worth would be $50,000.

If you have $50,000 in assets and $100,000 in liabilities, then you have a net worth of negative $50,000.

Why Calculate Your Net Worth?

Now that you know how to calculate your net worth, the next question is why should you do it?

I’ll use myself as the example here, since I have a couple of stories to share about this.

I started to track my net worth back in college.

That was over 20 years ago. I have tracked it every month since then.

Originally, I recorded it on a piece of paper and even created a chart on paper to graph it over time.

I still calculate net worth on paper, but I have since switched to Excel for the graph.

I was getting tired of re-creating the graph as I kept running out of room on a standard sheet of paper!

So how does calculating net worth help someone improve their finances?

Here are 3 ways.

#1. Wanting To Take Control

When I finished college, I had student loans and credit card debt.

As a result, my net worth was negative to the tune of close to $25,000.

I owed more than I owned.

I started working two jobs, primarily to pay off my credit cards, but also focused on paying down my student loans as well as investing a little each month.

Every month, my negative net worth would get smaller and smaller.

After about a year, I hit the “holy grail”. I had a positive net worth.

Calculating my net worth motivated me to improve my finances.

I wanted to see that ending number get to zero, and then become positive.

At the end of each month, I would get excited to see it change for the better.

One more point you should take away from this is that I didn’t pay off all of my debt in that one year but my net worth became positive.

How is this possible?

I was investing money along with paying off debt.

By investing some of my money, it was growing on its own.

While I invested $100 each month, at the end of the year, I had more than $1,200.

It compounded and earned dividends so I ended up with more.

If you want to improve your finances, you have to look at investing.

#2. Curbing The Urge To Spend

Around the time my net worth had turned positive, I started to notice some really nice new cars.

Nothing was wrong with my current car. I just wanted a new one.

The ironic thing is if I wasn’t tracking my net worth, I would have bought the car.

I looked at my positive net worth of $4,580 and realized that if I buy this $20,000 car, my net worth is going to be negative again.

While this thought may not make most people think twice, it made me reconsider the purchase.

I looked back at how hard I worked over the past year to get to this point.

I worked two jobs at close to 70 hours per week. One of which was in retail during Christmas.

How I didn’t end up with gray hair from that, I’ll never know.

I was essentially throwing all of that away for a car that I didn’t need, I wanted.

I ended up not buying the car and continued on the path of increasing my net worth.

By tracking my net worth, it made me question purchases that I otherwise wouldn’t question.

If it weren’t for my net worth, I would have bought the car and who knows what else and still be paying the price.

Calculating my net worth has made me a smarter shopper.

#3. Motivation To Reach My Goals

While I was motivated to get my net worth positive back in the day, calculating my net worth still motivates me today.

At the end of each month, I get excited to see what my net worth is.

I am a competitive person and I want to see my net worth increase each and every month.

I base many of my decisions on wanting to get further and further ahead financially so that I can be financially independent.

- Read now: Click here to learn 7 life lessons from the secret rich

- Read now: Discover the difference between the wealthy vs poor

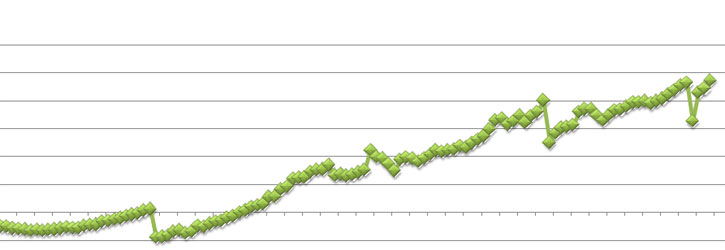

I look back at my chart of my net worth and see how over time I have increased it.

As I have invested more in the stock market, my money grows at a faster rate, increasing my net worth at a faster pace when the market goes up.

Of course, when the market drops, typically my net worth does as well.

But I know in time, the market will come back so I don’t worry.

Below is the chart of my net worth from the day I started through the end of last month.

The chart shows a steady incline with some bumps along the way.

The crazy part is that I can tell you what each large decline is.

Your net worth can be a visual guide for how far you have come.

It is easy to forget things in the fast paced world we live in.

Having a visual reminder can excite and motivate you to keep getting better.

Frequently Asked Questions

Figuring out your net worth is very basic, but there are some questions you might have about it.

Below I list some of the more common questions I hear regarding net worth.

Can I have a negative net worth?

It is entirely possible and not uncommon to have a negative net worth.

Negative net worth is associated with younger people since they tend to not have a lot of assets.

For example, if you are just graduating college, you probably have a large amount of student loan debt and not very many assets.

You can also have a negative net worth if your house is underwater.

If you are older and have a negative net worth, it can be a sign that you are handling money poorly and not saving anything.

As you age, your net worth should improve as you pay off your debt, make more money and save and invest.

Why is a negative net worth bad?

A negative net worth is bad because it essentially means that if you took everything you own, sold it and paid all of your debt, you would still owe money.

You are basically living beyond your means.

You need to get into the habit of saving money, building your assets and getting paying off your debt.

What should my net worth be for my age?

Financial Samurai put together an amazing post on The Average Net Worth for The Above Average Person.

This should be your guide to determining where you should be in terms of net worth.

While it might look overwhelming to get to these levels based on where you are today, it can be done.

You just have to put in some effort to be smarter with your money.

How should I calculate net worth?

There are three ways you can calculate net worth:

#1. Paper/Pen: this is the “old school” method. You would break the sheet of paper into two columns and on the left list out your assets and on the right, list out your liabilities. Then you would total them up and at the bottom complete the final calculation, assets minus liabilities to get your net worth.

#2. Excel: I created a free net worth template for you to use. Just enter in the amounts and let it take care of the math for you. Most of the categories are pre-filled for you. But if you find one is missing, you can replace an unused category with one you need or simply add a row.

#3. Online: Personal Capital is the gold standard for this. I highly recommend it. Just link up your accounts for free and it will crunch the numbers for you. Then in the future, whenever you want to see your net worth, just log in and Personal Capital will calculate it for you. There is nothing left to do on your end. You can learn more here.

Should I include personal property?

There are a few schools of thought on this one.

On the one hand, it makes sense to include it since it is a factor in what you are worth.

The problem is when you overestimate the value, which many people do.

Your belongings aren’t worth what you bought them for. They’re worth what you could sell them for.

The best way to handle personal property is to include it, but every year decrease the values by 3%, which assumes the inflation rate.

Should I include my house in my net worth?

Personally, I don’t include my house.

The reason is because I view my net worth as what I would have left if I sold everything I owned.

I wouldn’t plan on selling my house since I would keep it for a place to live.

Others might argue to include it as you can sell it and rent an apartment or buy a smaller house.

Including or not including your primary residence is not right or wrong, it is just personal preference.

I’ve always excluded my house and foresee that I always will.

Is it wrong if I ignore my personal property and house in my calculation?

Not at all.

In fact, I calculate three different net worth statements all of the time.

It wasn’t always like this.

At first, I calculated net worth as I detailed today, where I included everything.

But recently, I wanted to get a different perspective on my wealth.

I wanted to see how much I was worth when I just took into account my liquid assets like savings and investments and subtracted out the money I am in debt.

The point of this for me is to see how I am progressing towards building my wealth.

I do this by saving and investing, and not buying things which would increase my personal property.

I also perform a quick income to net worth ratio calculation.

This helps me to see that I am saving money and am on the path the financial independence.

At the end of the day, you have to determine what you want to know about your finances and build your net worth statement based on that.

At this time, I would just encourage you to start calculating your net worth.

In time, as you want other detailed information about your finances, you can make changes.

Do I include my 401k in net worth?

Yes, you include all of your retirement plans in your net worth.

Your retirement savings, including your 401k, traditional IRA, Roth IRA, etc. would be put in the asset section of your net worth statement.

Is my car an asset?

Your car is an asset and is included in the asset section.

However, your car is a depreciating asset.

This means it loses value over time.

Therefore, you cannot use the same value for your car every time sit down to calculate your worth.

Also, if your car has a loan against it, you need to put the loan in the liabilities side of your statement and the current value of the car in the asset side.

Do not subtract the loan from the value, as this done when you do the calculation of your net worth at the end.

Do I include jewelry in my net worth?

Yes.

Jewelry is a tangible asset that is included in your assets.

The same goes for art work, clothing, electronics, home furnishings and more.

Just make sure you use the fair market value when assigning a value to these items.

And make sure they don’t make up the majority of your assets.

Will my net worth tell me if I’m cash poor?

The great thing about your net worth is all the things it tells you.

And this includes if you are cash poor.

Being cash poor simply means you have very little liquid assets like cash and investments but a lot of personal property, like jewelry, clothing, home furnishings, etc.

- Read now: Discover 23 things money cannot buy

If you have a lot of stuff, your net worth may even be positive.

But this isn’t ideal.

You want the biggest percent of assets to be cash and investments.

These types of assets are what you will be living on come retirement.

So if you find you have very little in savings but a lot in physical items, you might want to take some time to reassess your priorities and start saving more and spending less.

How often should I calculate my net worth?

At the very least, you should calculate it on an annual basis, the same time each year.

For many, that would be year-end.

Ideally, you should calculate net worth quarterly.

I calculate net worth monthly and do it at the same time as my monthly budget.

I started doing this in college and enjoy sitting down at month end, making sure all of my accounts are balanced and nothing fishy is going on.

Since I have everything updated right then, I can quickly perform my net worth calculation.

Again, you don’t have to calculate net worth that frequently. Find what works for you.

What are some things I can do to increase my net worth?

The key to increasing your net worth is understanding that there are two components of it, assets and liabilities.

While you might think paying off debt won’t matter since you aren’t saving money, it does matter.

You are reducing your liabilities and as a result, are increasing your net worth.

Plus, debt carries interest.

So even if you aren’t adding to your debt, it is still slowly growing thanks to interest.

Here are some posts I wrote that will help you increase your net worth over time.

- Read now: Click here to learn how to slash your monthly expenses

- Read now: Discover how to save $100,000 quickly

- Read now: Learn 41 fun money saving challenges

- Read now: Find over 100 ways to save money starting today

- Read now: Discover the 15 steps to building wealth

Final Thoughts

It’s important to calculate net worth on a regular basis.

Doing so helps you to see your progress over time as to whether or not you are increasing your assets as you age, allowing for a secure future and retirement.

It can be a warning signal if you are spending too much as well.

I make a game out of it and work hard to consistently increase my net worth over time.

By not calculating net worth, you could be spinning your wheels, wasting time and not even know it.

But when you track your net worth, it can motivate and encourage you to reach your financial dreams.

I have never actually calculated my net worth. If I did I would surely use this as a guideline and my choice would be spreadsheets in Excel.

Nice breakdown Jon! It’s such a vital, yet simple way to see where you’re going financially. We do ours on a quarterly basis and just do a simple Excel spreadsheet to figure it out.

Good to hear you track your networth. It doesn’t take much time but tells you a lot about where you are heading.

You make a good point about the house, I have mine as part of my NW as I would sell it and go live somewhere cheap if I were really broke, or if I bought another house.

However I just put the price I bought for, not the price with all the renovations or what I think it is worth.

I think it’s definitely a personal preference. As long as you follow the same strategy every time you calculate your net worth, you shouldn’t have any issues.

I try and track my net worth a couple of times a year just to track our financial progress.

It’s amazing how many people do not get the “net” part of net worth. I see options applications everyday in which investors completely exclude debt and only include their gross numbers. Hopefully your formula will help.

I calculate net worth monthly. Considering how hard we work to improve our net worth, it’s certainly worth checking up on periodically!

I calculate my net worth monthly – it’s a great tool to see where I’m at!

I think my income statement is a little more beneficial in telling me where I’m going in terms of my finances though.

Thanks for sharing