THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

If your finances are a hot mess, there is no better plan to follow than Dave Ramsey’s Baby Steps.

These 7 steps give you simple, clear cut instructions on how to destroy your debt and start saving money.

Thousands of people have put in the hard work and been successful following these steps and are on their way to financial freedom.

Thousands more are working on completing these steps as you read this.

In this post, I will highlight each step and give you my opinion on why these steps work.

I also will point out any drawbacks I see and how you can make them even better.

KEY POINTS

How The Dave Ramsey Baby Steps Work

What Are The Baby Steps?

The Dave Ramsey Baby Steps appear in his book, The Total Money Makeover, and are what he talks about on the Dave Ramsey Show.

There are seven baby steps in total that help you go from financial disaster to financial master.

You work your way out of debt and begin to build savings.

By the end, you are completely debt free and have changed you finances for the better.

Here is a quick overview of each step.

Baby Step #1: Save $1,000 In A Starter Emergency Fund

The first baby step in improving your finances and building wealth is to create a starter emergency fund.

This emergency fund baby step requires that you save up $1,000.

The key here is to save this money as fast as possible.

There are two reasons you want to do this step fast.

First, by doing it fast, it forces you to think outside the box for ways to save money.

- Read now: Click here for 41 fun money saving challenges

- Read now: Learn 115 creative ways to save money

- Read now: Find out how to cut $7,000 from your monthly bills

And doing this will put you in a mindset that will help you with the rest of the baby steps.

Second, the debt you have is destroying your finances.

The sooner you can build up a $1,000 emergency fund and move onto the next baby step of paying off your debt, the better.

Baby Step #2: Pay Off Credit Card Debt

Now that you have some money to cover emergencies, you need to attack your consumer debt.

The goal here is to rid yourself of all debt, except your mortgage.

This includes student loans, personal loans, credit card debt, auto loans, medical debt, etc.

The best way to go about becoming debt free is to follow the debt snowball method, which Dave Ramsey recommends.

- Read now: Learn all about the debt snowball method

The idea behind using the debt snowball method is simple.

You focus on one debt at a time, and the debt with the smallest balance.

You put as much money as you can towards this debt while making minimum payments on all your other debts.

By paying your smallest debts first, you pay off that debt quickly, which motivates you to keep going.

Think about it.

If you have tried to pay off debt before, you probably pay a little extra money on all of your debt.

After a couple of months, you lose interest because your balances are not going down quickly.

It feels like you are running a race but your feet are stuck in the mud.

When you put all your attention to one debt, you wipe it out and this excites you.

You see the possibility of becoming debt free and keep going.

Baby Step #3: Save 3-6 Months Of Expenses In An Emergency Fund

Now that your consumer debt is gone, you need to take a step back and work on building a fully funded emergency fund.

This is because while having $1,000 for unexpected expenses is nice, in many cases, that amount of money isn’t going to get you very far.

A car repair or replacing your water heater is going to come close to wiping out your savings pretty fast.

As a result, you need to build up your emergency fund to cover more potential expenses.

In this regard, you want to save up so you have six months’ worth of living expenses.

The good news is this step should be fairly quick to complete.

This is because you have money now that was going towards your debt that you can now put towards building your savings.

Baby Step #3b: Save For A House Down Payment

The Dave Ramsey Baby Steps program doesn’t officially list this as part of the original seven baby steps, but has been added by Dave and others.

This step is for those looking to buy a house.

If you already own a house or are not interested in buying a house at this time, you can skip this baby step and move on to the next.

But if you are in the market for a house, your goal is to save at least 10% of the purchase price for a down payment.

Ideally, you want to have 20% saved so you can not only lower your monthly mortgage payment but also avoid private mortgage insurance (PMI).

The catch with this step though is you need to have the savings completed in 2 years or less.

The reason is because the remaining steps are still critical to get you on the path to wealth and the longer you spend on this step, the more harm you can do to your future finances.

Baby Step #4: Invest 15% In Retirement Account

Your next step in your wealth journey is to start saving for retirement.

Ideally you will save 15% of your income in pre tax retirement funds, which by the time you retire, should be a sizable nest egg.

The recommendation here is to invest in your 401k plan at work first, since you save money on taxes and if your employer matches your contributions, you get free money.

- Read now: See the pros and cons of 401k plans

If you do get an employer match, invest as much as you need to in your 401k to get the full employer match.

From there, you invest in another retirement fund, a Roth IRA.

This money is contributed after tax, which means you don’t save on taxes now, but it grows tax free into the future.

When you do take the money out, there is not any tax paid, making it tax free income for retirement.

Baby Step #5: Save For Children’s College Fund

This step is to save for your children’s college expenses so they do not become burdened by taking out student loan debt.

There is no set amount or percent of your income to put towards your children’s college fund here, just that you do it.

And when it comes to how to do this, you can opt for either an Education Savings Account (ESA) or a 529 college savings plan.

There are pros and cons to both college savings plans, so be sure to pick the one that makes the most sense for you.

Baby Step #6: Pay Off Your Mortgage

With baby step 6, you are working hard to pay off your home.

This is an incredible feeling when you no longer have to make monthly payments and the house is yours.

Add in lack of a monthly house payment and you will have a lot of excess cash every month to invest and build wealth.

Baby Step #7: Build Wealth And Give Back

The final step is to build wealth and give back to the less fortunate.

Use the extra cash in your budget to invest and save for your future.

You should also make it a point to tithe to causes you are passionate about.

Many people suggest you give away 10% of your income, but you can choose the amount that makes the most sense for you.

Why The Dave Ramsey Baby Steps Work

Overall, I think the general idea of Dave’s baby steps are great, and they work wonders.

There are a few reasons for this.

- Focus One Goal At A Time. We all have a lot going on in life and we tend to complicate things. By following the baby steps, you have one thing to do and you do not change it for any reason.

- Avoid The Debt Cycle. As you work your way through the steps, you learn more about money and good financial habits. This helps you to avoid getting yourself back into debt in the future.

- To Celebrate Progress. As you complete a baby step, you get to celebrate. They are mini milestones along the journey and having them is a great way to stay motivated.

Disadvantages Of Dave Ramsey’s Baby Steps

For anyone looking to get out of debt and start building wealth, Dave Ramsey’s Baby Steps are a great way to do it.

Are they perfect? No, but nothing in life is truly perfect.

Here are the issues or disadvantages I have with the baby steps.

#1. Never Address Root Cause Of Debt

I was in debt at one point in my life and I struggled to get out.

In fact, I was a classic case of the debt cycle.

I started to pay off debt only to end up in more debt down the road.

The reason this happened to me and happens to so many others is because they never get to the root cause of their debt.

They work hard at debt reduction only to find themselves back in debt a few months later.

You might think you are just bad with money or credit cards make it too easy to spend money.

These might be true, but they aren’t the reason why you spend money you don’t have.

In most cases, the real reason you get into debt is emotional.

You are unhappy with where you are in life, you are unhappy in your relationship, your career, or you are simply trying to fit in.

Until you acknowledge this, chances are you are going to end up back in debt.

For me, I thought I was bored and just enjoyed spending money.

But the truth is I was depressed that my life wasn’t unfolding the way I thought it was going to.

Added to that, I had low self-esteem.

Buying things made me feel better and allowed me to live in the fantasy of pretending my life was going as planned.

Once I admitted to myself my issues, I was finally able to break free.

So while I wouldn’t discourage you from following the baby steps, I would encourage you to do this.

Spend some time to figure out the reasons why you are in debt as you try to pay it off and come to peace with those issues.

#2. Put Off Saving For Your Future

When it comes to building wealth, your best friend is time.

The more time you let your money grow, the more it can grow into.

For example, if you invest $10,000 and it earns 8% annually, in 10 years it is worth $21,589.

Let it sit for another 10 years and it grows to $46,609.

And in 10 more years, your wealth grows to $100,626.

This is all because of time.

When you follow the Dave Ramsey baby step plan, you put off investing for retirement until you are debt free.

This could cost you 3-5 years or more, depending on how much debt you have.

Then it isn’t until step seven until you start saving more money for your future.

This can cost you a lot of money.

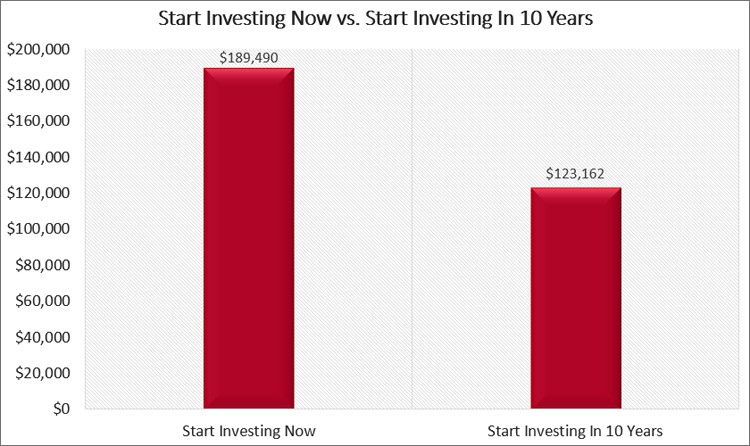

Let’s look at a quick example.

I start investing $200 a month today and do so for the next 25 years until I retire. I earn 8% annually.

You start investing 10 years from now, which means your investments have 15 years to grow until retirement.

You also earn 8% annually, but let’s say you are able to invest $350 a month.

In 25 years when we retire, here is how much wealth we built.

I have $189,490 and you have $123,162

That is a difference of over $65,000.

I end up with more money even though you contributed more than I did.

I invested a total of $60,000 and you invested $63,000 and yet I end up with more money than you.

As with the first drawback of the baby steps, this isn’t to say you shouldn’t follow them.

They are great for building a strong financial foundation and changing your life for the better.

I would just encourage you to work hard so you can get through them as quickly as possible so you can start investing and take advantage of time.

#3. Don’t Save Enough For Emergencies

Another downside to the baby steps is saving 3-6 months in an emergency fund.

Don’t get me wrong, any emergency fund is better than nothing.

Otherwise you run the risk of digging yourself into a deeper hole when financial surprises happen.

But back when these steps were first created, having this amount of money in savings for a job loss or other unexpected expense was acceptable.

But not today.

Gross household income and the cost of living has increased dramatically.

Plus there have been major economic downturns that have seriously impacted many households bottom line.

For example, look at 2020 or even 2008 to see why this amount is nowhere near enough.

Businesses shut down, people lost jobs, and the government took its sweet time when it came to assistance.

- Read now: Learn how to get back on your feet financially

- Read now: See how so many people ruin their financial life

Many people had their financial lives destroyed and many others are on the brink of disaster.

Had you saved 6 months worth of expenses, you would have run out of money if you faced major financial emergencies.

For peace of mind and financial security, I suggest you have at least 12 months worth of expenses in savings.

Ideally, you would have closer to 18 months.

While I’d love to say something like this will never happen again, the reality is it probably will.

And it’s because of this you need to follow the baby steps to rid yourself of debt and the monthly payments so you have more options in life.

The fewer debts you have, the more money you can save every month.

And the less you have in monthly bills, the less you need in savings to survive.

So work to get out of debt, but also make sure you build a fully funded emergency fund to cover unexpected expenses.

You will be more than thankful for this financial stability the next time a financial collapse comes along.

#4. No Defined Motivation

Another issue with Dave Ramsey’s baby steps is you are not asked to define what your motivation is at the start, including any financial goals you have.

Of course you want to get out of debt, but I’ve found when trying to achieve a goal, I need to be specific.

- Read now: Learn the best ways to stay motivated when paying off debt

- Read now: Discover the joys of debt free living

Saying I want to get out of debt isn’t good enough.

Yes it will motivate you at the beginning, but over time, as your financial journey continues, you will lose motivation.

By being specific with your reasons, you will find it easier to keep your motivation high and see your goal through until the end.

So start with your why and be specific.

Do you want to get out of debt so you can have the option to work at a nonprofit?

Or do you want to be debt free so you can retire early and travel the world?

Whatever your reason is, make note of it and use it as your motivation as you work to pay down your debt.

#5. Saving For Your Kids College Educations

I like the idea to save for your children’s education, I just wish this step was later in the series.

The reason for this is because there is nothing to help you afford retirement.

- Read now: Here is how much money you need for retirement

- Read now: Use these retirement calculators to see your financial needs

You have to get by on the savings in your retirement accounts, Social Security, and if you are lucky, a pension.

If you can’t make ends meet, you have to go back to work.

But when it comes to college, your kids can take out student loans.

They can get grants and scholarships.

They can even choose to go to community college first or even attend college part time.

My point is, I believe you should get your finances in order first and then start putting money away in your children’s college fund.

And if they have to take out a student loan, it’s not the end of the world, assuming they take out a reasonable amount.

Many people take out student loans and have no issue paying them back.

And then there is this.

If your financial house is in order and you realize you are ahead of the game, there is nothing stopping you from taking some of the money you have saved and using it to pay down or pay off your kid’s student loan debt.

#6. Paying Off Mortgage Early

Dave recommends paying off your mortgage early, but as with the last point, I think this baby step comes too soon.

I think one of the biggest mistakes people make is trying to retire when they have a mortgage.

If you have a $1,000 mortgage and you retire, you need an extra $12,000 a year in income as a result.

In a low interest rate environment, this could mean you take on more risk than you want to.

But I think the Dave Ramsey plan should be modified so the step to pay off your home is after the step to build wealth and give back.

As I mentioned above, time is your best friend when it comes to building wealth.

So instead of delaying it by a few years so you can be debt free, why not invest your money now?

You will get a much higher return in the stock market, making a smart move for your money.

And as your money grows into larger amounts, you could take a portion of it and pay off whatever amount remains on your mortgage.

Finally, when you pay off your home early, that money is tied up as equity in your house.

The only way to access it is to take out a home equity loan.

But then you have a debt payment again.

If you have the money in savings instead, you can use it if a major emergency comes up.

You can read more about this way of thinking in this post.

Frequently Asked Questions

I get asked a lot of questions about Dave Ramsey’s baby steps from readers.

Here are the most common ones.

Do Dave Ramsey’s baby steps work?

Yes.

They work for many people because they are simple to follow and help to keep you motivated along the way.

By keeping them simple, as in you do this and only this until it is complete, there is no guessing.

You follow each baby step, one at time before moving on.

What is the benefit of the baby step method?

The benefit of the baby step method is that you will achieve financial freedom.

You won’t be saddled with high interest debt or mortgage debt.

You will have a substantial balance in your retirement accounts and your household income will be more than enough to make ends meet.

Plus you will the peace of mind knowing that no matter the personal finance issue that comes your way, you will survive and thrive.

How long does each baby step take?

This varies person to person and how much credit card debt they have and the household income they earn.

Some people can run through them within 1-2 years.

Others will take up to 10 years to complete.

The question is how bad do you want to change your financial life?

If you want it really bad, you might be willing to work a second job to earn extra money so you can build your emergency savings quickly and use the income to pay down your debt.

You might also be willing to slash your living expenses to the bone so you can be debt free as soon as possible.

For others, they want to still be comfortable while working through the steps.

There is no right or wrong way here.

You pick what works for you.

What does Dave Ramsey say about renting?

He is all for renting.

In fact, you shouldn’t consider taking on mortgage debt until you know you are completely ready for it and have gone through the baby steps first.

This means not having any debt and having 10%-20% saved for a down payment.

Why does the debt snowball method work?

Using the debt snowball method works because it gets you to focus on one debt at a time.

You don’t have to do complicated math formulas. You just focus on the smallest debt and pay it off.

It also works because by paying off a debt quickly, you will get excited to see the progress you made.

As a result, you will be excited to tackle the next debt you have.

What is the downside to the debt snowball?

The downside to the debt snowball is typically you will pay more interest following this plan.

This is because you ignore the interest rate of your debt.

So if you choose your smallest debt, it won’t be costing you as much money because the balance is low.

Overall, you might end up paying a few thousand dollars more in interest.

While this might concern some people, remember this.

Your goal is to be debt free, not pay as little interest as possible.

So if paying a little more interest is a byproduct of reaching your ultimate goal, it isn’t the end of the world.

If you are interested, the alternative method is called the debt avalanche method.

This method has you organize your debt by highest interest rates.

You then focus on the highest rate card first and work your way down the list.

Is Dave Ramsey good for investing advice?

Dave Ramsey also offers investing advice for people who have successfully completed his baby steps.

I wrote a post about his investment philosophy and why I disagree with it.

The bottom line is, I recommend the baby steps for getting out of debt, but I do not recommend his investment advice.

Dave tends to support high fee mutual funds as well as a limited diversification approach.

Because of these and other issues, I don’t recommend you follow his detailed investing advice.

Final Thoughts

At the end of the day, the baby steps Dave Ramsey created to help people pay off their debt are a great resource to use.

When followed through to the end, not only will be have your debt paid off, but in many cases, reach financial independence.

There are very few criticisms with the baby step method and in most cases, they are minor.

The only caveat to this is I would recommend you build a larger emergency savings account.

This doesn’t need to be done before you move on the other steps either.

I would build 3-6 months in savings and as you move through the other steps, keep putting a small amount each month into your emergency fund until you get to 12-18 months in savings.

I know it sounds like a lot, but I’ve never heard someone complain they have too much money saved.