THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

Today’s post comes from Alex. He blogs over at Mutilate The Mortgage and is giving away a few free gifts just for Money Smart Guides readers. Head over to www.MutilateTheMortgage.com to find out how to pay off your mortgage in under 10 years.

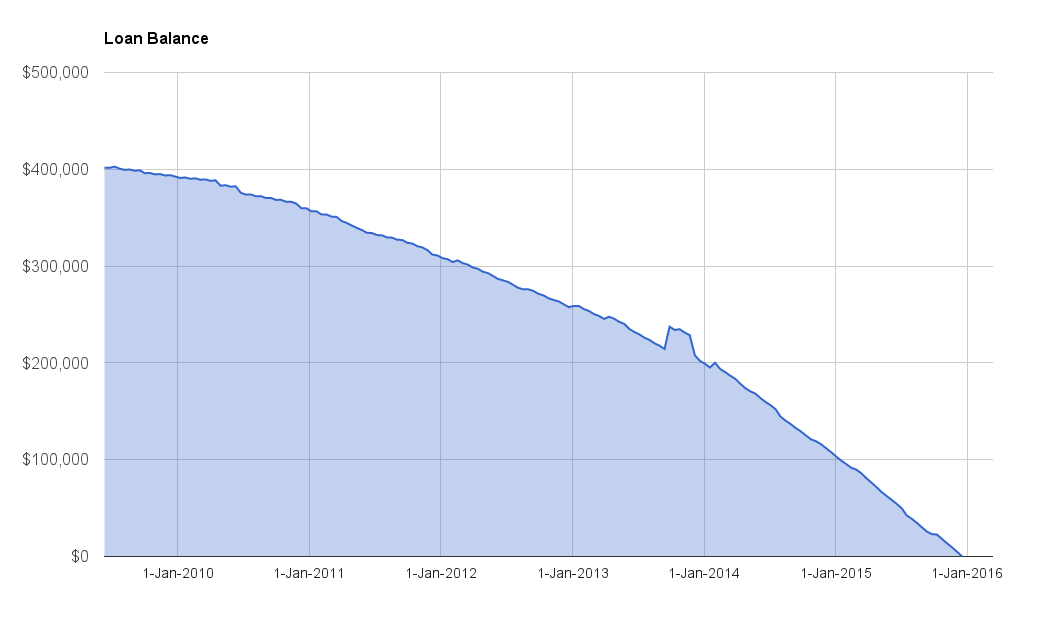

From start to finish it took us 6 years and 177 days or just shy of 6.5 years to completely pay off our mortgage and it’s changed our lives. We’re not alone either…

Started at $375k in Nov 2010. Currently remaining: $67k (May 2016). Tough going, but BEST DECISION EVER! – Martin

We paid off our $380K home loan in 3.5 years in 2010. Lots of hard work and sacrifice but it was worth it. – Huy

We now are 100% debt free. We own our house, our car, have no student debt and have never even used credit cards. Our financial standings are rock solid, our flexibility greatly increased and our happiness at an all time high with cash flowing in from everywhere like a fountain.

So do you have a mortgage? What would you do if it was gone in 7 years?

Think about it, you could easily have one parent stay at home with the kids all year round. You could plow that money towards your savings for early retirement whilst still having plenty to travel abroad every year. You could feel safer knowing that even if you lose your job you’ll always have a roof over your head.

Now we all want to put more money towards our mortgage but money is boring and everything seems to be working out fine anyway… so why bother? Instead we tell ourselves that it’s “normal” or that our loan “isn’t that bad and Bob’s is WAY higher than ours so it’s fine“. How often have you heard:

Mortgage debt is good debt

I’d say most of us have at some point, but just because home loans have a lower interest rate or are more socially acceptable (unlike credit cards) doesn’t mean the interest repayments are any less real. A lot of people really worry about their mortgages everyday in the back of their minds. Winners on the other hand destroy them and move on to bigger and better things which is exactly what we’ve done and what you can do too.

By paying our loan off super early we saved $316,562 in interest. In the final year we were paying over 5 times the standard loan repayment amount, automatically and I’m not telling you this in arrogance.

See how much money you can save by playing with the calculator below.

I’m telling you all this to show you that we’re nothing that special in fact. We’re not earning $400,000 CEO salaries every year, we haven’t received any inheritances. We don’t even buy lottery tickets let alone have won any jack pots.

This isn’t a scammy, get rich quick scheme that only works for the people on top or the 0.0001% of people that “make it”. This result was achieved through specific, repeatable actions which you can do too and the results are achievable for everyone, even if you’re on a single income, even if you’ve got children.

Heck, even if you are BOTH those things there are winners out there using this knowledge and getting ahead.

So what have I learned and how can you benefit from my journey over these years?

The Most Important Things I Learned

Straight off I’ll get right into the absolute core of it all:

1. Set your repayments higher and make them automatic. This is THE most critical thing you need to be doing. You can scheme, wrangle and fiddle around with a million things for years and years but without throwing large percentages of your income at your mortgage consistently… it’s going to do virtually nothing to your loan. I’m not going to lecture you on not buying lattes or your favorite take out but money needs to be allocated to your mortgage.

The single biggest thing I learned is to ignore virtually all the “experts” tips and instead focus all your effort on finding ALL available extra money and pushing that to the mortgage. I’m not talking about that once off $2,000 bonus or tax return or whatever, I’m talking about looking at your income and setting up an automatic, reoccurring payment to your mortgage that is made up of a sizable chunk.

Think $1,000, $2,000, $4,000 on top of your normal mortgage payment every fortnight. How you get that extra money is something I cover in detail at Mutilate The Mortgage but for now I’d just like to focus on the mortgage part.

To throw this serious cash at it regularly use “recurring payments” which is a feature you can setup in your online banking account. For example John might get paid every month on the 15th. He would then set it up so that on the 16th 50% of his pay is automatically transferred to his mortgage or offset account as an extra mortgage repayment.

At some point his normal mortgage repayment will be taken out too but this way he is adding more to his mortgage and still has control to increase/decrease the automatic extra repayment if needed.

Whilst it can look different for different countries and banks, below is an example of how you would do it using the bank ING. First Login, then click on the “Transfer & pay” menu on the left, then choose “Transfer Funds”.

By setting it up this way you achieve your goals at the same time as it all being automatic, hassle free and as painless as possible. After a while you don’t even notice it and you can just keep enjoying your life while you systematically cut your mortgage down.

2. Motivation. Whilst it sounds like something you may shrug off, it is in fact very critical. Even if you’re destroying your mortgage and only needing 5 years to pay it off… that’s still 5 years you need to keep up your motivation because without it there’s sure to be something else to tempt your money away. You can know all the tips and tricks but if there is no motivation, no reason for you to do something you will simply do nothing and not care.

Find out why you want to pay off your mortgage faster and put that reason in a very visible spot so you never forget it. Then keep reminding yourself of that reason every few months by imagining what that future will look like. Maybe use that reason as your “transaction description” so you see it each time the money is automatically transferred.

Want to be mortgage free before you have children? Are you just sick and tired of being in debt? Whatever it is make sure it’s clear and on display so you’re continuously motivated to reach your goal. We had this reason always on display in the spreadsheet we used to manage our finances and although we had our extra mortgage repayments all automatically setup it still helped a lot over the long years it took to accomplish.

3. Cutting costs and increasing efficiency. The more of this you do, the sooner you will pay off your mortgage, it’s that simple. It also has the added benefit of often simplifying your lives and making you happier. On top of all that, it’ll mean that when you save for retirement you won’t have to save as much which means you can retire earlier.

After setting up the initial automatic payment your main focus should be on finding MORE available income by cutting costs, earning more income and increasing efficiency. When you trim or save on your bills, up the amount of your automatic payment. When you get a raise or new job paying more, up the amount of your automatic payment. I posit most people can strive or get to pushing 70% of their after tax income towards their mortgage and a number of people even go further than that.

I recently heard a great quote that I think applies well here:

I do the things you won’t, so I can get the results you can’t

Don’t settle for “saving 5%” or other minuscule targets most financial experts trumpet, you CAN do better! Winners do better. Australia is one of the most expensive countries to live in on Earth with our two main capitals (Sydney and Melbourne) being 20th and 21st on the worldwide cost of living survey with only New York and Los Angeles being higher up.

Even with that high cost of living we and others regularly hit 70%+ savings rates so push the bar up and aim for something that’s more inspirational!

Summing It Up

Summing up all the knowledge I’ve gained over the past 7 years ends up being quite simple, but don’t let the simplicity deceive you as there’s great power in being simple, precise and consistent – it’s how great things are always achieved.

- Set automatic extra repayments and make them BIG

- Stay motivated

- Focus your energy on always increasing those automatic repayments

Overall it was a long and involved process for us. We basically started from scratch searching all the Google pages for all the tips and tricks as well as learning what everything meant and how it all interacted but ultimately none of it is really that necessary.

If we had just done those three things above from day one I believe we could have paid it off in under 5 years not 6.5. Those three lessons accounted for about 98% of our effort and the results speak for themselves. I’d do it again in a heartbeat too as who doesn’t like taking $315K+ back from the big banks???

Spot on! Paid off $161k in 6 years. Our success what paying every two weeks consistently and throwing every extra dime at principle. The extra went after the regular two week payment so it brought that principle total down penny for penny. We won’t have the interest deduction but the extra money can now be better used. Do it if you haven’t already – you can do it!!

Like the author, I’m a fellow Aussie (Sydneysider) who paid off the mortgage in 6.5 years. Coincidentally, it was 6 months before the baby came. We should’ve been able to pay it off a year earlier except we purchased an investment property.

The most useful technique for us was using an offset account, where our income is automatically deposited into the home loan account and interest is reduced by the same amount. It took a lot of self-discipline not to spend the increasing amount of money but it did pay off in the end.

The most important thing was getting into the habit of saving. This was really tough because I spend everything I earnt in my 20s. But, it’s possible!

Good work. Many people always say you can make better returns on your money elsewhere, which may be true, but I think for those focused on paying down their mortgage, it’s never ever a wrong or bad decision.

100% debt free – wow! I’m hoping to achieve that in two years time..

Nice strategy. It’s possible to pay 400k mortgage is a short period of time. Thanks for sharing the strategy.