THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

If you are thinking about taking out a loan against your 401k, there are a lot of things you need to think about.

On the surface, borrowing money from your retirement money might sound like a smart financial decision.

But you need to know that there are risks involved.

And by not properly weighing these risks, you could easily put your retirement savings in jeopardy.

In this post, I am walking you through the biggest 401k loan pros and cons so you can make the best financial decision for yourself.

In the end, you will have a solid understanding of the benefits and the risks and will be able to make a wise decision.

10 401k Loan Pros And Cons You Need To Know

401k Loan Pros

There are a lot of advantages to taking out a 401k loan.

I am not listing all of them, just the ones that will have the biggest impact on your decision.

#1. No Need To Qualify For A Loan

If you have ever taken out a loan before, you know the process takes time.

And depending on the type of loan you are looking to get, you may need to gather a lot of financial documents.

All told, qualifying and getting approved can take anywhere from a few days to a few weeks.

With a 401k loan, this is not the case.

All you have to do is fill out a form and you are done.

There is no lender involved.

The reason it is so simple is because it is your money.

You can use the money to pay off credit card debt, medical expenses, pay off your student loan, buy a car or house, or use it for financial hardship withdrawals.

With a typical loan, you are borrowing the money from a bank, so they do a lot of work to make sure you will pay it back.

Since it is your money, this step is skipped, making the process much faster.

You may even be able to get it the next day.

#2. Does Not Affect Your Credit Score

When you take out a loan, the creditor will complete a credit check by pulling your credit history and checking your credit scores.

These checks will have a minimal impact on your credit score.

But if you end up taking a loan out, it will go on your credit report and will have a larger impact on your score.

If you miss a payment, your score is going to drop.

And by simply taking out a loan, it will affect your debt to income ratio, which will also have an impact on your score.

With a 401k loan, you don’t have to worry about it impacting your credit score.

Because you are borrowing money from your retirement plan, nothing will show up on your report.

The credit reporting agencies won’t report if you miss a payment or are late with a payment.

And it will also not have an impact on your debt to income ratio either.

#3. Lower Interest Rate

Depending on the loan you are taking out, interest rates will vary greatly.

For a mortgage it could be as low as 3%. For a traditional loan to buy a car a personal loan, it could easily approach 10%.

And don’t get me started on credit cards. The annual percentage rate on these will be as high as 17%!

If your score is low, the interest rate will be higher.

A 401k loan has a typical interest rate is set at the prime rate plus 1-2%.

The prime rate is what most banks charge their absolute best business borrowers.

In other words, you are getting a great deal.

As of this writing the prime rate is 3.25%, so the rate you are looking at with your loan is between 4.25% and 5.25%.

You also get favorable repayment terms as well, which are up to 5 years to pay the retirement loan back.

#4. Pay Yourself Back

When you take out a 401k loan, you are borrowing the money from yourself, not a bank.

As a result, when you pay back the money, you are paying yourself back, not a bank.

This means you will be putting any money you borrow from your retirement plan back into your account.

And any interest will also go back into your retirement account as well.

This helps to offset one of the biggest drawbacks to 401k loans that I talk about shortly.

#5. Quickly Get Access To The Money

I briefly mentioned this above, but a great advantage to taking out a retirement plan loan is that you get the money fast.

In some cases, you get the money the next business day.

This is great for people looking to use the money in a time sensitive manner.

For example, if you need the money fast for home repairs or to buy a car, you won’t have to worry.

401k Loan Cons

While the benefits listed above are great, there are consequences of borrowing from your 401k.

Here are the biggest drawbacks that you need to consider.

#1. Limits To The Amount You Can Borrow

There is a rule limiting how much money you can borrow from your retirement account.

In most cases the maximum loan amount is limited to $50,000 or 50% of the vested balance.

This means the amount is based on the money that is yours, not the money your employer contributed into your account that has not vested yet.

So if you have a $25,000 balance in your 401k plan the most you could borrow is $12,500.

- Read now: Click here to learn the average 401k plan balance

- Read now: Learn 10 401k plan pros and cons

And this is assuming the entire amount is fully vested.

If your vested account balance was only $7,000 then that is all you could withdraw.

In other words, you are not going to get a loan to buy a house in most cases.

Of course this is not a rule across the board.

Some plans do not allow for loans at all.

Each retirement plan is different so reach out to your plan administrator or benefits administrator to know what the rules are for your plan.

#2. Issues When Switching Employers

You took out a loan to buy a car and then you get laid off.

What happens to the repayment of the loan?

It no longer is looked at as a loan but as a taxable distribution.

And instead of having up to a 5 year repayment period, you now need to repay the unpaid balance by the time you file your tax return or face penalties.

If you don’t pay the outstanding balance back in full, then you pay Federal Income Tax on the amount at current rates for ordinary income tax.

In addition to that, you are charged a 10% early withdrawal penalty.

This means if you are in the 25% tax bracket, you are being charged a 35% fee on this loan.

And since money isn’t taken out of their paychecks to repay the loan, most people won’t pay it back.

The result is a lot less money saved for retirement.

This situation also applies if you switch jobs as well.

So make sure you think long and hard about your job situation with your current employer before taking out a loan.

#3. Loss Of Bankruptcy Protection

With other consumer loans and high interest debt, if you get into trouble financially, you can discharge most of the debt you have when you file for bankruptcy.

But in the case of a 401k loan, you don’t have this option.

Even if you file for bankruptcy, you will still be responsible for paying back your outstanding loan balance.

This is because you didn’t take the loan from a third party. You borrowed the money from yourself.

#4. Loss Of Investment Growth

This is the biggest drawback of 401k loans.

While it is great to borrow and pay yourself the interest, you are losing out on a large amount of potential long term growth from investing in the stock market.

You will also hear people talk about this as opportunity cost.

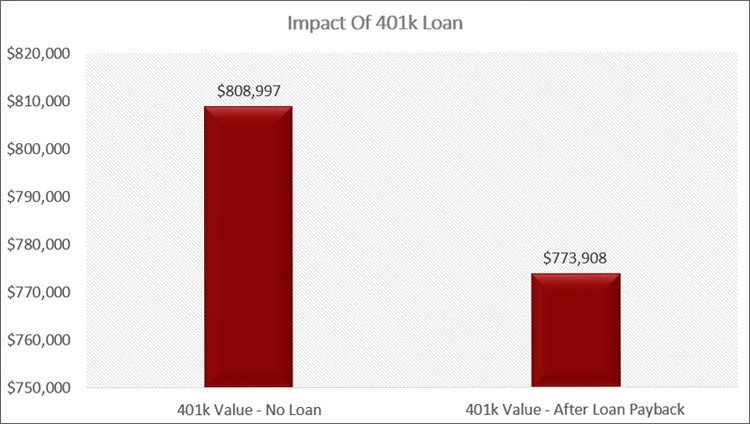

Let’s look at an example.

Assume you have $50,000 in your 401k and it earns 8% annually.

We will also assume you are contributing $2,500 a year into the plan.

In 30 years, your 401k is worth $808,997

Now let’s say you borrow $25,000.

You pay the loan back over 5 years and you are paying 4.25% interest.

At the same time, you are contributing $2,500 a year into the plan.

The value of your 401k after 30 years is $773,908.

By borrowing money from your retirement plan, you cost yourself over $35,000 of potential growth.

This is because the money you took out for your loan misses out on compound growth and market appreciation, lowering your ending balance.

Also the rate of return you earn on your money is more than the interest you are paying yourself.

So while you do make up some of the loss by paying interest, it is not enough to offset the loss of growth.

#5. Additional Fees And Taxes

As great as it is to get your money fast, not worry about your credit and get a low rate, these are countered by fees.

Most times when you borrow from your 401k plan, you are going to pay fees.

In some cases, a lot of fees.

These can be processing charges for taking out a loan and also include annual maintenance fees as well.

These fees will vary by plan sponsor, so it is critical you ask about any and all fees before you fill out the paperwork.

For example, processing fees and loan origination fees could total $150.

And this is before you even get your money.

The annual maintenance fee could run an additional $150 a year until the loan is paid back.

If you take the maximum 5 years to repay it, that is $750!

Finally, you get hit with taxes that most people won’t tell you.

When you make retirement contributions to your 401k plan, you do so with pre-tax dollars.

This helps you to lower your taxable income and save you money.

But when you are repaying your 401k loan, the payment is made with post-tax dollars.

This is true even if you pay using payroll deductions.

And even worse, there is no distinction made when you do retire and begin to withdraw the money from your account.

This means regular contributions and your loan repayments will be lumped together, and you will owe income taxes on your distribution.

This means you will be paying tax twice, once on the money you earn and are using to repay your loan and again when you take your distribution.

Also, understand that the interest you are paying yourself is not tax-deductible either, so you don’t get to write it off on your tax return.

Final Thoughts

At the end of the day, taking out a 401k loan is a big decision.

While it might seem to make sense today, the long term effects on your retirement cannot be ignored.

While most financial experts would recommend you not take out loans against your 401k, each situation is different.

Take the time to consider all of your options so that you don’t make a decision you will later regret.