THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

A little more than a year ago, I plunked down $81,000 of cold hard cash and bought my first rental home outright.

A little more than a year ago, I plunked down $81,000 of cold hard cash and bought my first rental home outright.

No mortgage, no bank, no hassles. It was glorious.

The first question you might have is, “How on earth did you get yourself into a position to buy a house with cash?”

Well, that’s really not the purpose of this article, but I’ll give you the quick gist of the last 6(ish) years of my life:

- I was going backwards financially and got mad. I made a plan and I paid off $40,000 in consumer debt.

- I figured, “why stop here?” and I paid off my steal-of-a-deal house (that I bought for $75k).

- I stayed intense and built up $90,000 in savings (it’s pretty easy when you have no bills).

- I searched through thousands of ads to find the perfect deal, and bought an $81,000 house.

Wow, those bullet points make it sound so simple. And to be completely honest, it really was.

Sure, scrimping and saving and living below your means isn’t always a blast, but buying a house with cash sure is!

So that was the how. Now it’s time for your second question:

“WHY on earth would you buy a house with cash? Don’t you know it’s wise to use other people’s money?”

Blah, blah, blah…

Table of Contents

5 Benefits Of Buying A House With Cash

When I bought this house with cash last year, I was heckled by nearly every person I spoke to about it.

“Derek, really? Don’t you know that it’s smarter to use the bank’s money? And interest rates are so low right now, why WOULDN’T you take out a loan?”

Basically, everyone looked at me with that, “wow, you must be stupid” face, and it was really starting to tick me off.

Deep down in my soul I KNEW it was smart to use cash, but why? How could I convince everyone that I wasn’t as stupid as they thought I was?

Here are the 5 reasons I came up with.

#1. I’m Not Paying Interest

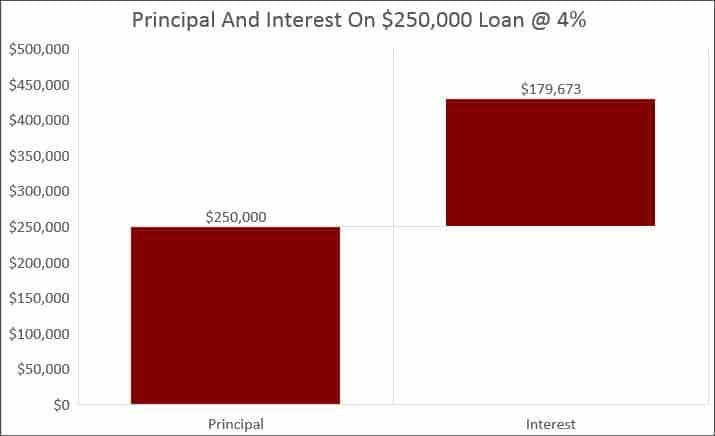

If you bought a $250,000 house today and scored a heck of an interest rate of 4%, guess how much you’d end up paying for the house over that 30-year loan period?

$430,000! Yikes!

You know how much I end up paying when I buy the home with cash? Exactly $250,000.

For all you finance “whizzes” out there, you’re probably thinking, “This guy is such a simpleton. He’s not even considering the time value of money! Inflation on average is nearly 4%, so why not borrow at the inflation rate and use today’s dollars to earn more on something else?”

The answer I have for you is two-fold.

- The inflation rate in the last 10 years has been 1.8%

- The banks are massive corporations. Many highly paid intellects figure out the interest rates that make them the most money. Do you really think you’re going to win by playing their game? Who’s the simpleton here?

By plunking down $250,000 in cash, I’d effectively be paying $324,000 in inflated dollars.

Still sounds a lot better than $430,000 to me!

Savings = $106,000

#2. No Appraisal Needed

When I bought the rental, I didn’t need to pay an appraiser for their estimate of the home’s worth.

Appraisal costs are basically mandated by the bank so you can let them know that the house is worth more than the amount you’re borrowing from them.

It’s insurance that the bank is requiring YOU to pay.

I knew I was getting a good deal based on my hundreds of comps over the past year. There was no need for an appraiser to come tell me what I already knew.

Savings = $350

#3. Ridiculously Low Closing Costs

Our closing costs on the house were $532. I laughed when I saw it.

Most of today’s closing costs are really just admin fees from the bank to process your paperwork:

- Origination fee (a large flat fee from the bank for the overall processing)

- Credit report fee

- Loan application fee

- Private mortgage insurance

- Initial interest

- Title services

- Property taxes

You know what I paid for? A small amount of property tax and title insurance. That’s it.

Savings = $2,000

#4. Reduced Price

The house we purchased was a bank-owned foreclosure and it was November. It had been sitting on the market since July when it was initially priced at $120,000, and was recently just dropped to $89,900.

Banks aren’t in the business of selling homes. It’s just a by-product of their mortgage lending business and they get stuck with it occasionally.

I knew this bank didn’t want to take care of this house through the winter time. If I gave them a cash offer, I was betting that they’d bite.

My first offer was $80,000. They countered at their full asking price of $89,900 which I thought was pretty strange, but I kept playing their game.

I countered at $80,000 because if they weren’t going to move, why should I? They countered at $86,500. I countered with an all cash offer of $81,000. They accepted.

I’m fully convinced that cash got me a deal of at least $5,000. They knew that if they accepted my offer, they were going to sell the house.

There wasn’t a third party that had to get in the way.

Savings = $5,000

#5. Simplicity

Paying for a house makes the initial process simpler, but it also makes life more enjoyable after the house is purchased.

Think about it:

- I have no mortgage payment to make each month.

- I don’t have to deal with the escrow fund (management of this is typically terrible).

- I can change home insurance companies simply and easily, without permission from the bank.

- I pay my property tax just once a year.

The only thing I need to worry about each month is picking up the $1,200 rent check and taking it to the bank. Love it!

Savings = Roughly $0

#6. Peace Of Mind

I saved the best for last. Peace of mind.

The bank has absolutely no idea that our rental house exists, and that makes my heart smile.

So many people have paid their mortgage faithfully for years, had something happen like a sickness, job loss, you name it, and the bank took away their home.

I refused to become one of those statistics.

And you know the best way to avoid it? You keep the bank’s grubby hands out of your home!

Savings = Priceless

Final Thoughts

If you want the ultimate peace of mind, commit to buying your next home with cash.

Sure, people will think you’re crazy, but it’s honestly one of the best feelings in the world and I highly recommend it.

Author Bio: This post has been written by Derek Sall, owner of LifeAndMyFinances.com. His motto: Get out of debt, save money, and be rich!

—–Editor’s Notes——

I love everything about this idea! I’ve found that many times when people are questioning my decisions, it is the best move to make.

The best way I can put it is this quote by Dave Ramsey:

Live like no one else, so later on you can live like no one else.

It is a powerful idea. If you can learn to live on just what you need and save as much as you can, you are going to have more wealth and more options than you can imagine in the coming years.

This isn’t to say you have to be miserable today. You just have to understand what you value and spend your money there and forget about everything else.

If you can do this, you will find you are happier today than you ever have been and, in the future, you will have the means to do whatever it is you desire.

Take the first steps to living like no one else today so you can live like no one else tomorrow.

Here are some great articles to get you started!

- Learn the best way for getting out of debt once and for all

- Here is the simplest way to become rich

- 115 simple ways to save money starting today

- Learn how to earn 5% raises every year

I have over 15 years experience in the financial services industry and 20 years investing in the stock market. I have both my undergrad and graduate degrees in Finance, and am FINRA Series 65 licensed and have a Certificate in Financial Planning.

Visit my About Me page to learn more about me and why I am your trusted personal finance expert.

A $1200 rent check on a $81K house? Works to a 17.8% cap rate! Wow!! How did you get this kinda deal and what desperate local market offers this deal and yet is strong enough to get you credit-worthy $1200/month renters?

Hi TFR. I just have to say….I love where I live. 😉 A low cost of living, great deals on fixer-uppers, and high rent rates.

To be fair, we put approximately $9k into the house for an all-in cost of $90k. But, with just that little bit of work, the house is now valued at about $125k.

The key to buying this house at such a low price – the inside was UGLY, it had been on the market for a while (with regular price reductions – so it wasn’t an immediate deal that people jumped on), and it was bank owned. They loved my cash offer. Oh, and we bought in November – I knew the bank wouldn’t want to take care of this house through the winter.

Congrats on buying in cash. It’s just not done often enough. Everybody thinks it’s impossible. You showed them it is.

For me, the best part is signing at closing. Sometimes, I only sign one document. I love it!

Paying off my primary residence and buying houses for cash got me to financial freedom! Keep it up. That rental income snowballs quickly.

Thanks for spreading the word on this!!!

Love it! It’s good to have confirmation from other from time to time. Typically, people just tell me I’m dumb because I’m not using other people’s money (OPM) – you know, the broke people that I refuse to listen to.

I’m fascinated by this! Especially impressive is the $500 closing cost total. We have plans to purchase some rentals and are hoping to pay cash as well. I am curious about one thing: to get the inflation adjusted amount of savings ($324,000) did you take the $250,000 and determine a future value? I want to do some similar calculations.

Not one, but 2 houses paid in cash…you rock!

HI Kathryn. Thanks for the kudos! I basically used the 10 year inflation rate of 1.8% over the course of 30 years. Just plunk these figures in an investment calculator (Dave Ramsey has a good one) and you’ll get your future value.

This was a really good read. When we paid off our mortgage, we got many similar naysayers. The majority of them argued “What about the TAX deduction!?!?!” That was when I learned most people have absolutely no clue what a tax deduction is. So we had to slowly and simply explain to them how we would rather NOT pay the bank $5k a year in order to save $1k in taxes. We were also able to suggest that we tithe $5k a year to the church and still keep our tax deduction, while giving no interest to the bank. Most people’s minds were blown.

EXACTLY! Fricken tax deduction people…. they make me so mad sometimes. 😉

Nice read! Congrats on your debt-free purchase. I’m also against the idea of excessive debt. But a completely debt-free rental property has the disadvantage of potentially a lower than necessary net rental yield. Why not buy two rental properties each with a 50% mortgage and juice up returns a little bit? Most successful REITs have leverage, Otherwise, they couldn’t be competitive. I invest in real estate through a few Private Equity funds and they use moderate leverage, too.

But again, I’m completely against the leverage mayhem from the bad old days in 2007/8.

Cheers!

“Why not buy two rental properties each with a 50% mortgage?” Did you really just ask that after reading this article? Let’s see, my closing costs would have been about $5,000 more, I’d be paying interest, my risk would be way higher in the event that I couldn’t pay for them….etc etc. With borrowing comes risk, which often isn’t factored into the great math of the financiers.

Debt free investing is the way to go.

Yup, I most definitely said that after reading the article.

Yes, you’d pay interest, but the rental income from the second property is large enough to pay the mortgages on both properties.

The additional closing cost from two properties is easily recovered with the additional rental yield after less than a year (even net of the mortgage)

Another reason to carry a mortgage: lawsuit protection. You have less money on the line for each house if someone sues (e.g. tenant or someone who fell on the sidewalk). Also, the mortgage on a property is already somewhat of a poison pill for greedy lawyers.

And more on risk: Since you can own more properties with leverage you also smooth out the cash flow volatility from vacancies

But again: I’m not telling you how to run your business. I’m just saying what I observe in the real estate business: Successful RE investors work with leverage. People who used too much leverage got bankrupted in 2008/9. But people who want to avoid leverage at all costs leave money on the table. Which I like because there will be more deals for me to invest in.

Cheers!

ERN

Buying cash brings the huge safety of NOT having any payments to make! This is a huge plus, especially once retired! Congrats on the new move, I wish we were mortgage-free!!!

Hi XYZ. Start working at paying off that debt and it can happen for you too! It happens faster than you think if you make it a defined goal.

Congratulations on your purchase! To be honest I’m still more like a mortgage “fan” under 3-4% rate, but it’s definitely a superb buy considering the rental fee you can get. 1,200 per month is an excellent return. And I really like the way you negotiated with the bank. Well done! 🙂

Why? Why pay 3-4% if you don’t have to?

Because the expected return on investment is higher. Taking the average historical roughly 7% real return of the stock market, that still gives you a 3-4% extra above inflation vs the mortgage. It’s more like the feeling of living debt free could be the biggest advantage of buying cash.

You explained it beautifully!! Well said Samantha!

Great job!our plan is to buy a house cash too. We have $90k in our house fund now and still unsure when we will pull the trigger. My husband moves around a lot for work. We have been looking to buy around Atlanta since we are familiar with the area and houses are cheap but unsure about how the rental market is there. Any insight on how you go about figuring all that out? Thanks 🙂

If the location is farther away from you than 1 hour, I wouldn’t recommend it. Start with property that’s close and manage it yourself for the highest returns.

Good stuff Derek! Remind us again where you can get such a good deal? So much more expensive here in SF!

Sam

Hi FS! I scored this deal in good ‘ol West Michigan. I love it here! The wages are decent, the cost of living is cheap, and the beaches are fantastic! 🙂

Congratulations on getting your finances done and being able to buy a house cash in the end. It’s never stupid to buy a house cash especially when you don’t let the house and have somebody else pay the debt.

Hi Thomas. Thanks for the congrats! There are just so many benefits to buying a house with cash. I doubt I’ll ever take on debt again! In fact, we’re almost ready to buy rental house #2! Can’t wait!

I bought an investment house to flip several years ago with cash. I saved a fair amount in junk fees and other closing costs, and the closing time was cut in half. For a flipper, those advantages are huge, because time is money.

Razmaspaz makes a great point about opportunity costs. In my current home, I had enough cash to put 66% down. Being newly divorced and single parent at the time I bought it, I chose to put all the cash in my home rather than just put enough for 20% down and put the rest in an emergency fund. I was too focused on keeping my monthly payment down to be thinking clearly. But after the 66%, the remaining balance wasn’t enough to fund a traditional first mortgage, so I let them talk me into a HOME EQUITY loan for the balance. Not only did it raise my rate a full percentage point, but it has kept me from being able to refinance my loan at a lower rate, because in this state you can only refinance a home equity loan with another home equity loan, and those rates are always higher than conventional mortgage rates.

I shudder to think what opportunities I have missed out on because of that one lapse in judgment. It’s cost me untold thousands of dollars. But maybe someone reading this will learn and not make the same mistake.

Mortgage loans have their pros and cons; one of the cons being the fact that mortgages are usually very emotional decisions that can keep the borrower from realizing a better bang for his or her buck somewhere else.

Interesting point Sagar. Thanks for sharing! It’s not always easy to keep a level head through a divorce. I know, I’ve been through it. I hope that you’ll soon be able to pay off the mortgage though, and then you can stop worrying about it!

Buying a house for all cash is great if you can raise the money. Unfortunately, in states like California, you would be hard pressed to find a decent house (i.e. a house that doesn’t require additional fix-up costs) at any price even close to what you paid.

For some people, saving up $81,000 could take many years. In the mean time, if they had bought the same house and only put up a 20% down payment, in 5 years, assuming a 7% increase in the value of the home, the return on the original down payment would be over 600%, versus only 40% for the all cash investment.

Hi Fred. I wouldn’t assume an increase in home value. That’s just an added bonus if it happens (we’ve all seen the housing market plunge just a few years ago).

Yes, it’s probably fairly impossible to buy a home with cash in California. That’s the price that some people choose to pay to live there. Notice I said choose to pay…. It’s their choice to live there.

As for the $81,000, yes, that can take a while. But, with a $75,000 salary with no bills other than utilities, insurance, and food, it can be done in about 3 years. Then the next rental can be purchased 2 years later. Than the third one in nearly one year… It really snowballs quickly once you get the ball rolling.

Check out my Rental Property Wealth Calculator and see for yourself — http://lifeandmyfinances.com/2017/01/rental-property-wealth-calculator/

Good article..!!

I think paying for a house in cash makes you a very appealing buyer and can get you a better deal. I agree with the main advantage that you mentioned is not to worry about mortgage payments. You can lose your peace of mind over those payments not to mention the hassles of getting a mortgage.

Definitely. I get so stressed out with debt, and I have such peace without it. To not owe anyone anything is a beautiful thing!

For anybody who criticizes your choice to buy the house outright, just offer to compare your net worth to theirs. I’m guessing 9 times of 10 you’ll come out on top.

Haha, I’ll have to try that.

You’re right though. Our net worth is really jumping lately – nearly $100,000 a year. I don’t even earn that much with my salary, but with the rental income, my website, and the increase in property values, it’s right there. Crazy how it all works.

Very impressive, I can’t believe how much you saved in interest alone! This isn’t a method you hear of often, but if you have the means, it definitely sounds like the better option. Thanks for sharing!

You’re welcome, Heather! I’m glad to share it, because you’re right – nobody EVER promotes investing in real estate with cash! And you know why? Because it’s not good for anyone except the investor! 😉